It’s difficult to overstate the effect that the release of ChatGPT and Nvidia‘s (NASDAQ: NVDA) incredible growth had on the investing world and the broader economy. Going into 2023, most investing talk was about when the recession would come and how deep it would be. It seems like a long time ago now, but it isn’t. Not only did the country avoid a recession, but the markets made new all-time highs. Nvidia stock is a revelation, but the 234% run in the last year has many investors looking elsewhere.

Companies are investing billions in artificial intelligence (AI) technology. The race is on. Here are three companies with tremendous potential.

Is SoundHound AI a good investment?

Automated ordering is popping up across the county at quick-service restaurants (QSRs) like White Castle, Applebee’s, and others. I believe most QSRs and quick-stop stores will use this technology within a decade because it will increase efficiency and allow the companies to keep prices reasonable, which is critical given the recent high inflation.

You may have used SoundHound AI‘s (NASDAQ: SOUN) speech-recognition technology already, as there are over 10,000 active locations as of Q1 2024. The company also provides AI-powered “Smart Answering” tech for customer service departments and in-vehicle voice systems. SoundHound holds hundreds of patents and has a massive addressable market.

With SoundHound’s awesome potential comes significant risks for shareholders as well. Take a look at these metrics, which I will break down below.

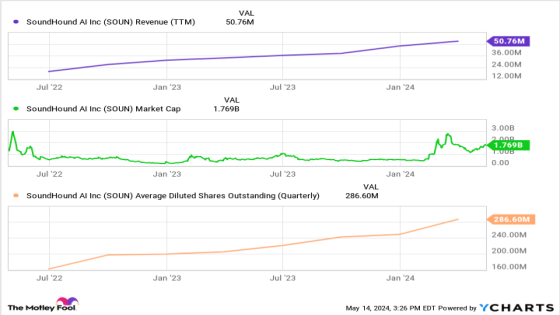

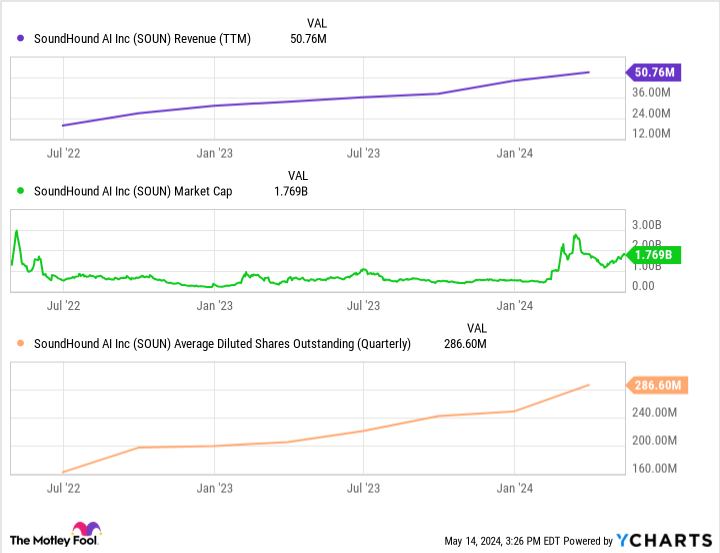

First, we have the revenue in purple. SoundHound reported $11.6 million in sales in Q1 (+73% year over year) and $51 million over the trailing 12 months. Sales have more than doubled since 2021. The growth is terrific, but this level of sales may not justify the $1.8 billion market cap, labeled in green, for an unprofitable company.

Finally, since SoundHound is unprofitable and not cash-flow positive, it uses equity financing (selling stock) to raise cash for marketing, research and development, and general expenses. As you can see by the orange line, the number of outstanding shares increased from 199 million at the end of 2022 to 286 million last quarter. The more shares there are, the less portion of the company each share is worth. Equity financing put SoundHound on solid footing with $226 million in cash, but it may need more before turning a profit.

Voice-recognition technology is the future of ordering at QSRs, and the technology will continue to advance for automobiles. There will be big winners in this space. While it is a risky investment, SoundHound could be one of them.

What is Google doing with AI?

Alphabet‘s (NASDAQ: GOOG) (NASDAQ: GOOGL) Google Search has enjoyed an incredible run of search engine dominance, but things are changing fast. The introduction of ChatGPT and the evolution of large language models (LLMs) mean that Google Search must evolve, which is precisely what Alphabet is doing. In 2014, the company acquired AI research company DeepMind and merged this team with its “Brain team” in 2023 to form Google DeepMind, whose mission is to research, develop, and bring AI solutions to the market.

The company is undertaking many initiatives to remake itself as a major player in AI. Here are a couple of examples:

-

The generative AI virtual assistant Bard, which rivals ChatGPT;

-

PaLM2, designed for higher-level analysis, code writing, and conversational comprehension;

-

The Tensor Processing Unit (TPU), designed to train Chatbots and other AI programs efficiently; and

-

Its latest, most advanced LLM, Gemini, which integrates with Bard and is capable of “sophisticated reasoning” and advanced coding.

Alphabet is also on firm financial footing. The company reported a 15% increase in sales in Q1, reaching $81 billion, a 32% operating margin, and $29 billion in cash flow from operations. The balance sheet shows a cash and investment balance of $108 billion — plenty of money to fund operations and invest heavily in research and development.

The largest risk to Alphabet is heavy competition from Microsoft, which has invested heavily in OpenAI (the company that made ChatGPT) and other AI programs. However, the market will probably be big enough for both companies to be successful. The stock has a price-to-earnings (P/E) ratio of 26.6, close to the five-year average of 27. The P/E drops to 23 on a forward basis, making Alphabet a highly profitable, innovative company with long-term upside potential.

GOOG PE Ratio data by YCharts

Why is Arm Holdings stock up?

Arm Holdings (NASDAQ: ARM) stock has risen more than 80% since its September 2023 initial public offering. We use Arm’s semiconductor technology daily, even when we don’t realize it. According to the company, 99% of all smartphones use Arm CPUs, and 287 billion Arm-based chips have been produced to date. It’s important to know that Arm does not manufacture semiconductors; it designs the “architecture” for advanced chips and licenses the technology to others. It makes money through license fees and royalties on products sold.

Arm is a very attractive company to me since it doesn’t have major capital expenditures for factories and equipment like manufacturers. Instead, it is a chip company with margins like a software company. Arm reported non-GAAP gross and operating margins of 95% and 42%, respectively, in fiscal 2024. It also converted 29% ($947 million) of its $3.2 billion in sales to free cash flow. These are tremendous numbers. For comparison, Alphabet had a 22% free-cash-flow margin over the last 12 months.

ARM Free Cash Flow data by YCharts

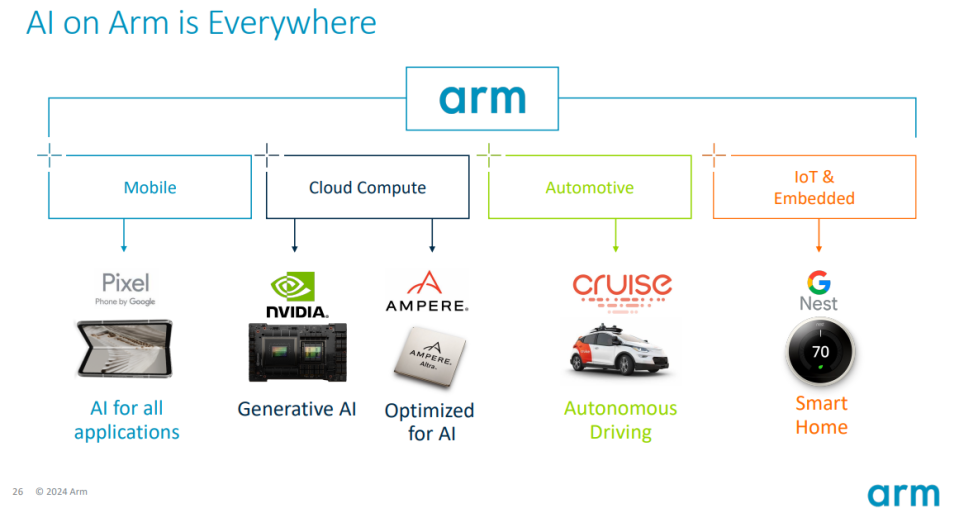

As shown below, Arm technology is used in multiple AI-enabled arenas:

Arm stock isn’t easy to value since the company has been public for less than a year and has no apples-to-apples comparable. The recent enthusiasm suggests that long-term investors can be patient and utilize dollar-cost averaging to lower risk and take advantage of pullbacks.

Competition in the AI space is intense. Some companies will be massively successful, rewarding shareholders in the process. Keep a keen eye on SoundHound, Alphabet, and Arm.

Should you invest $1,000 in Arm Holdings right now?

Before you buy stock in Arm Holdings, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Arm Holdings wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Bradley Guichard has positions in Alphabet, Arm Holdings, and Nvidia and has the following options: long January 2025 $2 calls on SoundHound AI. The Motley Fool has positions in and recommends Alphabet, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

3 Artificial Intelligence (AI) Stock Picks With Incredible Potential (Hint: They’re Not Nvidia) was originally published by The Motley Fool

Source Agencies