After a few years of disappointing stock performance, Walt Disney (NYSE: DIS) is looking a bit more magical these days. The stock has climbed 12% over the past year, and the company has made progress in cutting costs and boosting growth. In the most recent earnings report, the entertainment giant even reported profitability for the entertainment streaming business — Disney+ and Hulu — and forecast profitability for its entire streaming business in the fourth quarter of this fiscal year.

All this sounds great, and Disney makes an interesting buy — but another consumer stock makes an even better recovery and growth investment right now. This player, like Disney, attracts vacationers — and struggled when it had to halt operations during early pandemic days.

In more recent times, though, this company has demonstrated its ability to streamline operations, become more efficient, and bring in customers at record levels. And over the past year, this stock has soared more than 30%. Let’s take a closer look at this unstoppable growth player to buy instead of Disney.

Carnival’s early pandemic problems

I’m talking about the world’s biggest cruise operator, Carnival (NYSE: CCL) (NYSE: CUK). As mentioned, the company experienced rough waters in the early days of the COVID-19 pandemic, with a halt to cruising leading to a net loss — and explosive growth in debt.

But Carnival took action by tackling efficiency and costs. Moves included eliminating old ships and replacing them by new, fuel-efficient ones; developing a new port positioned to support fuel-efficient itineraries; and focusing on ways to boost cruisers’ onboard spending. The company also made paying down debt a priority, and importantly Carnival addressed variable-rate borrowings, prepaying more than $1 billion early last year. This makes Carnival less vulnerable in a higher interest rate environment.

In the first quarter of last year, cash from operations turned positive, making a focus on debt repayment possible. And thanks to ongoing positive cash from operations, Carnival can continue along this path of debt reduction.

On top of the cost cutting and streamlining, Carnival also is seeing enormous demand, showing that people’s interest in cruising remains high — and the pause early in the pandemic was just a temporary one. In the most recent quarter, Carnival’s booking volumes reached a record high even with cruises priced higher than they were a year ago. And total customer deposits came in at a first-quarter record of $7 billion.

Carnival’s record revenue

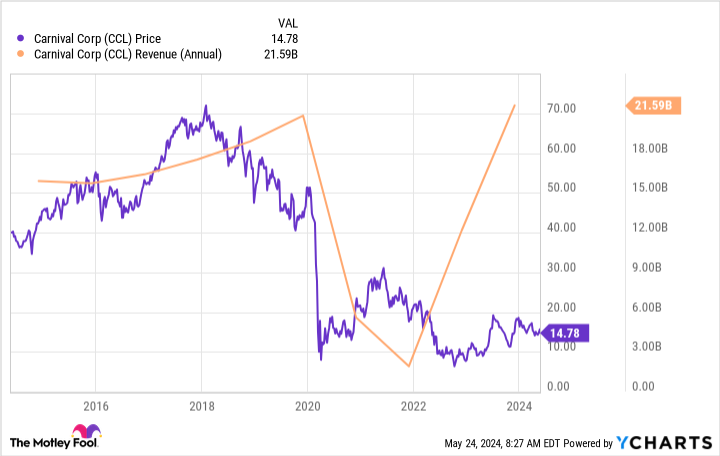

Demand for Carnival cruises helped the company report record first-quarter revenue of $5.4 billion and a $500 million improvement in the bottom line compared to the year-earlier period. So, there’s plenty of evidence that Carnival not only is recovering from its difficult early pandemic days, but the cruising giant also is entering a whole new era of growth.

Meanwhile, even though Carnival’s shares have shown momentum in recent times, they’re still far below pre-pandemic highs. And at the same time, revenue has returned to and even exceeded pre-pandemic levels.

All this has left Carnival’s shares trading for 0.84x sales, close to their lowest level ever by this measure. Disney shares also are trading at reasonable levels, but at about 2x sales they’re pricier than those of the cruise leader.

So even though Disney is inexpensive and future prospects look bright, investors looking for an unstoppable growth player should forget about the entertainment powerhouse for the moment — and instead turn to Carnival.

The cruising company is cheap, has made important progress along its path to recovery, and has demonstrated that demand for its cruises is strong even amid higher prices. And many of the efforts Carnival has made to spur recovery — such as focusing on fuel efficiency — should support earnings growth over the long term.

All of this means that right now, with Carnival shares trading for a bargain, is the perfect time to get in on this growth story and potentially win as the company reaches its recovery goals — and delivers explosive growth over time.

Should you invest $1,000 in Carnival Corp. right now?

Before you buy stock in Carnival Corp., consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Carnival Corp. wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Adria Cimino has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Walt Disney. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.

Forget Disney: Buy This Unstoppable Growth Stock Instead was originally published by The Motley Fool

Source Agencies