The Switzerland market recently experienced a downturn, influenced by concerns over U.S. interest rates, with the benchmark SMI index closing lower. Amidst these fluctuations, companies with high insider ownership can offer potential resilience and alignment of interests between shareholders and management, which could be particularly appealing in uncertain economic times.

Top 10 Growth Companies With High Insider Ownership In Switzerland

|

Name |

Insider Ownership |

Earnings Growth |

|

Stadler Rail (SWX:SRAIL) |

14.5% |

23.4% |

|

VAT Group (SWX:VACN) |

10.2% |

21.2% |

|

Straumann Holding (SWX:STMN) |

32.7% |

21% |

|

Swissquote Group Holding (SWX:SQN) |

11.4% |

14.3% |

|

Temenos (SWX:TEMN) |

17.4% |

14.7% |

|

LEM Holding (SWX:LEHN) |

34.5% |

10.1% |

|

Sonova Holding (SWX:SOON) |

17.7% |

10.4% |

|

Sensirion Holding (SWX:SENS) |

20.7% |

78.3% |

|

SHL Telemedicine (SWX:SHLTN) |

17.9% |

96.2% |

|

Arbonia (SWX:ARBN) |

28.8% |

78.2% |

We’ll examine a selection from our screener results.

Simply Wall St Growth Rating: ★★★★☆☆

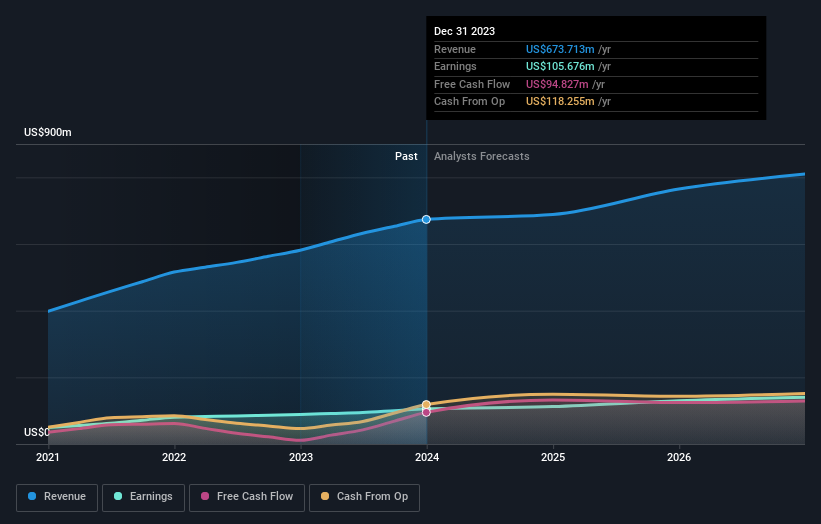

Overview: INFICON Holding AG specializes in developing instruments for gas analysis, measurement, and control, operating both in Switzerland and internationally, with a market cap of approximately CHF 3.52 billion.

Operations: The company generates revenue primarily from its global supply of instrumentation for gas analysis, measurement, and control, totaling $673.71 million.

Insider Ownership: 10.3%

INFICON Holding AG has shown a solid financial performance with a revenue increase to US$673.71 million and net income rising to US$105.68 million in 2023. While its earnings growth is forecasted at 9.85% per year, slightly ahead of the Swiss market average, this rate does not reach the high-growth benchmark of over 20%. The company’s Return on Equity is expected to be strong at 27.6%, indicating efficient management and potentially attractive to investors focusing on corporate governance and insider stakes.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sonova Holding AG, with a market cap of CHF 17.54 billion, is a global provider of hearing care solutions for adults and children across the United States, Europe, the Middle East, Africa, and the Asia Pacific.

Operations: Sonova’s revenue is primarily derived from its Hearing Instruments segment, which generated CHF 3.36 billion, and its Cochlear Implants segment, contributing CHF 282.40 million.

Insider Ownership: 17.7%

Sonova Holding AG, despite its high level of debt and highly volatile share price in recent months, trades at 35.6% below its estimated fair value, suggesting potential undervaluation. Its revenue growth is moderate at 7.1% per year, outpacing the Swiss market’s 4.4%, with earnings expected to grow by 10.42% annually—above the market’s 8.3%. The company’s strong projected Return on Equity at 27.4% highlights efficient capital management amidst a backdrop of stable financial performance with CHF 609.5 million net income reported for the fiscal year ending March 2024.

Simply Wall St Growth Rating: ★★★★★☆

Overview: VAT Group AG operates globally, specializing in the development, manufacture, and supply of vacuum valves, multi-valve units, vacuum modules, and edge-welded metal bellows; it has a market capitalization of approximately CHF 14.77 billion.

Operations: VAT Group’s revenue is primarily derived from its Valves segment, which generated CHF 782.74 million, and its Global Service segment, contributing CHF 172.87 million.

Insider Ownership: 10.2%

VAT Group AG, a Swiss company with high insider ownership, is poised for robust growth. Earnings are expected to increase by 21.17% annually over the next three years, outpacing the broader Swiss market’s 8.3%. Similarly, VAT’s revenue growth forecast at 15.5% annually also exceeds the market average of 4.4%. Despite this promising growth trajectory and a significant projected Return on Equity of 39.1%, the company’s share price has been highly volatile recently, which may concern some investors.

Key Takeaways

Contemplating Other Strategies?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SWX:IFCN SWX:SOON and SWX:VACN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source Agencies