Many people follow billionaire hedge fund managers to get investing inspiration — and that makes sense. After all, those investors have turned their own funds into billions. The hedge funds they operate usually have high minimum investment requirements that pose an insurmountable barrier to entry for the average retail investor. But these funds have a legal obligation to report their investing activity each quarter in a Securities and Exchange Commission (SEC) filing called the 13F, which anyone can access.

There are some caveats to the approach of seeking stock picks in those reports, though. One is that many of these funds invest in hundreds or even thousands of stocks, using a combination of diversification and risk-management strategies. After all, they are called “hedge” funds. Main Street investors can’t mimic the behaviors of a fund that has billions of accessible dollars. Moreover, 13F forms don’t have to be filed until 45 days after the end of the quarter they cover, so any information they convey is coming at a significant time lag.

So while it wouldn’t make sense to attempt to use that data to copy a hedge fund, individual investors can still see what the pros are doing and decide whether or not some of those moves are right for their own portfolios.

In the first quarter, billionaire David Tepper of Appaloosa Management opened a new position in JD.com (NASDAQ: JD) stock, buying 3,649,863 shares. The Chinese tech stock is down by 72% from the high it touched in 2021, so this is a bet on a recovery. Should you follow Tepper into this stock?

Setting itself apart in a competitive industry

JD.com is a Chinese e-commerce giant that competes with Alibaba and PDD‘s Pinduoduo. It operates in a fiercely competitive market, and all these companies tout their low prices and their logistics capabilities. JD.com’s revenue reached a peak in 2022, but it has since slowed down. Although macroeconomic and geopolitical factors have been affecting its deceleration, its rivals have been growing much faster, and investors have been disappointed in JD.com’s performance.

JD.com has a large direct-to-consumer core segment and controls a massive share of China’s home appliance and electronics market, but it’s actively focused on generating more business from its technology and supply chain platforms. It’s scaling up these businesses to recruit new clients and stake a large claim on the overall Chinese retail market. And like anything that scales, that creates a wider web that enhances itself. The company can reach more locations faster and with better cost efficiency, leading to improved margins and profits.

Management’s guidance forecasts that business will improve in 2025, and that JD.com’s revenue growth will outpace China’s overall retail sales growth as it delivers robust results on the bottom line. The stock also pays a dividend that yields 2.6% at the current share price.

Is this an attractive entry point for retail investors?

JD.com stock may have bottomed out when it hit a low earlier this year. Though it has been sliding since a few days after it reported Q1 earnings last month, it has been on an upward swing since early March, and that may reflect that investors are ready to take a chance on it again.

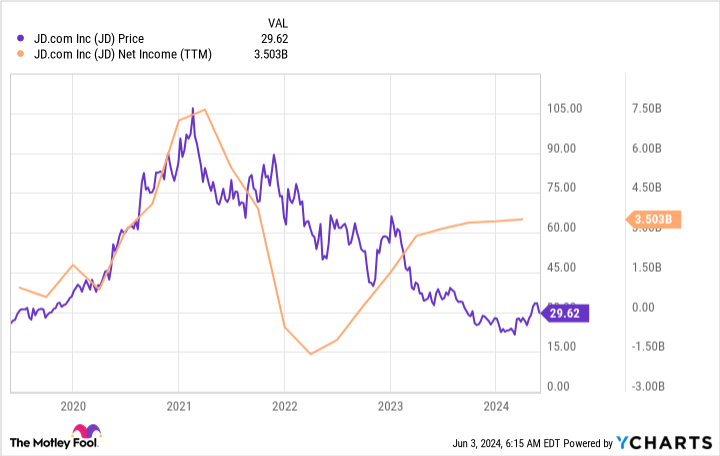

At the current price, JD.com stock trades at a price-to-earnings ratio of about 13 and an incredibly cheap forward 1-year price-to-earnings ratio of 8. Back in Q1, both of those metrics were even lower, and Tepper and his team may have recognized that, at those levels, it was too good a deal to pass up. As you can see from this chart, the stock’s price previously moved in line with the company’s net income. But as its net income has recovered, the share price has not. There’s a lag, but the market should eventually catch up, which is why this stock may look like an opportunity.

But is it an appropriate opportunity for individual retail investors? Actually, I think this is an investment best left to the pros. Hedge fund managers are paid precisely to make riskier plays, and they have backup strategies (in other words, hedges) to increase their likelihood of overall success no matter what happens to one stock. But investors who have strong appetites for risk and well-diversified portfolios may want to open small positions in JD.com now.

Should you invest $1,000 in JD.com right now?

Before you buy stock in JD.com, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and JD.com wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $713,416!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JD.com. The Motley Fool recommends Alibaba Group. The Motley Fool has a disclosure policy.

Billionaire David Tepper Just Made a Once-in-a-Generation Bet on This Stock. Time to Buy? was originally published by The Motley Fool

Source Agencies