Are you on the hunt for a new “forever” dividend stock? If so, you’ve probably already stumbled across beverage behemoth Coca-Cola (NYSE: KO). The company’s not only paid dividends like clockwork for decades now, but has also raised its annual dividend payout every year for the past 62 years. You could certainly do worse than plugging into this blue chip ticker while it’s yielding just a tad over 3%.

You could also do a little bit better, however. Shares of rival PepsiCo (NASDAQ: PEP) offer a slightly higher dividend yield at this time, while the stock itself may offer more upside potential.

PepsiCo isn’t the company you might think it is

Don’t freak out if you already own a stake in Coke. You’ll be fine. It’s a proven player, too.

If you’ve only got room for one or the other in your portfolio right now, however, the 16% sell-off PepsiCo shares have suffered since peaking in early May makes it the better prospect at this time. At least some of this setback is simply the result of the stock going ex-dividend in the meantime, as well as recent reports that Dr. Pepper has caught up with Pepsi as the nation’s second-favorite soda. Perhaps (or perhaps not) coincidentally, Pepsi’s veteran marketing chief, Todd Kaplan, also recently stepped down to pursue an external opportunity.

Are you surprised at the optimism in the face of obvious challenges? It would be a little surprising if at least some investors weren’t. PepsiCo’s supposed to be a reliable No. 2 player behind dominant Coca-Cola, after all.

Except, PepsiCo’s not just a beverage business. It’s not even mostly a beverage business. PepsiCo is also the name behind market-leading snack chip brands Frito-Lay and Quaker, which collectively account for nearly 60% of the company’s revenue, and an even bigger proportion of its profits. Pepsi’s failure to keep Dr. Pepper in check means even less given that each still only accounts for just a little more than 8% of the United States’ soda market. Making it even less meaningful is the fact that PepsiCo is also a licensed bottler and distributor of the Dr. Pepper brand. It’s benefiting from the rival drink’s expansion as much as it’s being hurt by it.

In other words, Dr. Pepper’s growth isn’t exactly a sign that Pepsi’s in trouble.

PepsiCo’s secret long-term growth edge

Perhaps more important to income-minded investors is the nature and quality of PepsiCo’s business. It is more diversified than Coca-Cola’s even if it is a lower-margin operation. But, it’s also a lower-risk, higher-reward proposition.

How so? The explanation lies in the way Coca-Cola and PepsiCo are different.

Contrary to a common assumption, Coke does very little of its own bottling these days. It’s spent the past several years selling its bottling operations to localized franchisees, which buy its flavored syrups and use its brand names. The model works, but its bottling partners are also customers trying to turn a profit of their own. The company and its affiliates aren’t always necessarily on the same page when it comes to selling goods.

This is in contrast with PepsiCo, which remains more intimately involved with the production of its products — drinks, and snacks, the latter market of which PepsiCo dominates here and abroad. Although the company utilizes third-party bottlers and food producers when merited, it also outright owns several production facilities. While these facilities can be expensive to operate (leading to the aforementioned narrower profit margins), this sort of structure ultimately gives PepsiCo better control of the entire procurement-to-distribution process.

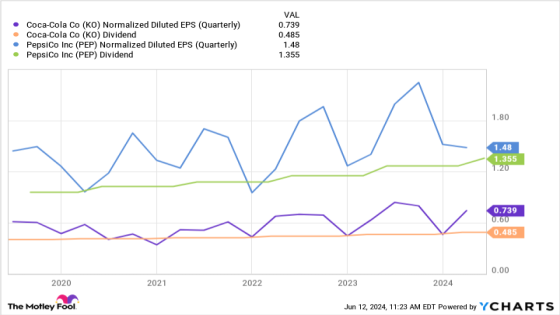

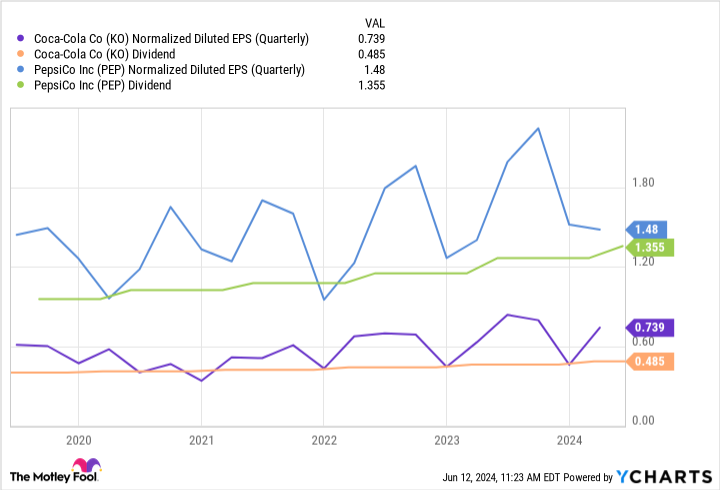

In a crowded, competitive market like food and beverages, these unseen, qualitative details make a difference. The numbers confirm this. Although Coca-Cola has grown its per-share profits since regrouping from the initial impact of the COVID-19 pandemic, PepsiCo has grown its bottom line even more. Moreover, PepsiCo’s per-share dividend has outgrown Coke’s during the same time frame.

It should be noted that at least some of PepsiCo’s superior per-share metrics can be chalked up to the fact that the company is buying back its stock at a faster clip than its archrival.

The reason, however, is irrelevant. PepsiCo is creating more shareholder value than Coca-Cola, and is operating a snacks-led business that’s capable of continuing to do so for the foreseeable future. Its 52-year streak of annual dividend increases isn’t exactly in jeopardy, either.

Bigger doesn’t necessarily mean better

Again, if you’re instead a fan of Coca-Cola’s bigger size, don’t sweat it. You’ll do fine with that pick as well.

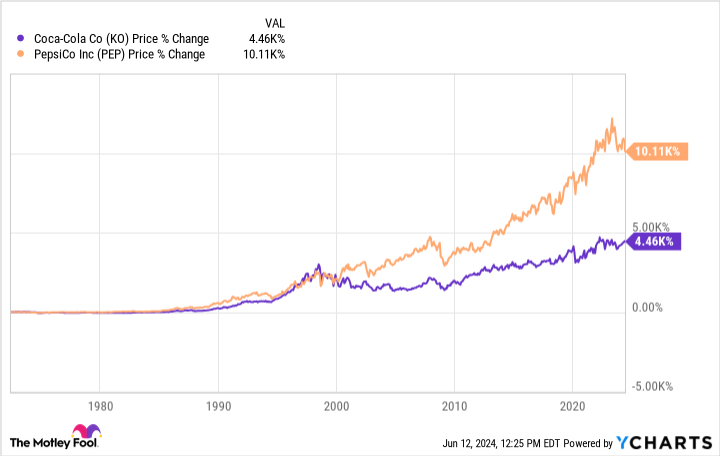

Just know that you may be able to do better with an investment in PepsiCo while its forward-looking dividend yield stands at 3.3%. Not only is it growing its dividend payments and profits at a faster clip than its bigger beverage competitor, PepsiCo stock’s also been dishing out more capital appreciation than Coke shares have for a long while now.

Bottom line? Believe what your eyes and the numbers are telling you. As unlikely as it seems that Coca-Cola isn’t the best dividend stock pick in the beverage business, PepsiCo is the better option here specifically because — despite most assumptions — drinks aren’t its core moneymaker. Dominating the snacks business means it’s been able to grow more than most people would have ever imagined.

Should you invest $1,000 in PepsiCo right now?

Before you buy stock in PepsiCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PepsiCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $740,886!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Magnificent S&P 500 Dividend Stock Down 16% to Buy and Hold Forever was originally published by The Motley Fool

Source Agencies