In May, 51 million retired-worker beneficiaries took home an average Social Security check totaling $1,916.63, which works out to $23,000 on an annualized basis. While this might not sound like a game-changing amount of money, the average retiree would struggle mightily without their guaranteed monthly benefit.

Over the last 23 years, national pollster Gallup has surveyed retirees to gauge their reliance on Social Security income. Between 80% and 90% of respondents have consistently leaned on their payout as a “major” or “minor” income source. In other words, a majority of retired workers might not be able to cover their expenses if Social Security didn’t exist.

Considering how important this program has been for more than eight decades to the financial well-being of our nation’s aging workforce, it’s no surprise that the annual cost-of-living adjustment (COLA) is the most anticipated announcement for beneficiaries.

What, exactly, is Social Security’s COLA and how is it calculated?

In simple terms, Social Security’s COLA is the mechanism that accounts for inflation. If you were to put together a basket of all the goods and services seniors regularly buy, and the price to purchase these collective goods and services increases, benefits should, ideally, rise by a commensurate amount to ensure no loss of purchasing power. COLA is the tool that determines how much benefits should increase from one year to the next.

In the 35 years following the mailing of the first Social Security retired-worker benefit in January 1940, cost-of-living adjustments were disbursed on an arbitrary basis by special sessions of Congress. Not a single COLA occurred into the entirety of the 1940s, and only 11 total adjustments were made prior to 1975.

Beginning in 1975, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) became the annual inflationary measure for America’s leading retirement program. Every major spending category and subcategory within the CPI-W has its own respective weighting, which allows the index to be whittled down to a single figure each month. This makes it really easy to determine if prices are rising (inflation) or falling (deflation).

Although the CPI-W is reported on a monthly basis by the U.S. Bureau of Labor Statistics (BLS), the trailing-12-month CPI-W readings from the third quarter (July-September) are the only figures used to calculate Social Security’s COLA for the upcoming year.

If the average third-quarter (Q3) CPI-W reading in the current year is higher than the average CPI-W reading from the same period last year, inflation has taken place and beneficiaries are poised to receive a larger Social Security check. The percentage difference between these average Q3 CPI-W readings, rounded to the nearest tenth of a percent, determines how much benefits will increase in the upcoming year.

Social Security’s cost-of-living adjustment hasn’t done this since the late 20th century

For the 51 million retired-worker beneficiaries currently taking home a monthly check, the 2025 Social Security COLA could be extra special. Though it’s not currently on track for an eye-popping year-over-year increase, it’s nevertheless on pace to do something that was last seen in 1997.

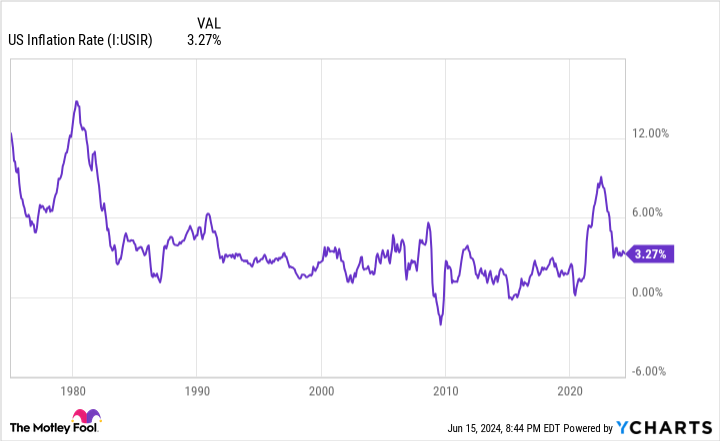

On June 12, the BLS released the much-awaited May inflation report, which showed that the CPI-W had increased by 3.3% on a trailing-12-month (TTM) basis. That’s down one-tenth of a percent from the TTM increase in the April inflation report.

Based on this new round of inflation data, the Social Security policy analysts at The Senior Citizens League (TSCL), a nonpartisan senior advocacy group, are forecasting a 2.57% COLA for 2025 (which would round to 2.6%), which is down from a previous forecast of 2.66% following the release of the April inflation report. Over the last 20 years, the average cost-of-living adjustment has been 2.6%.

However, even average COLAs have been tough to come by on a consistent basis since this century began. Deflation resulted in no COLAs in 2010, 2011, and 2016, while the 2017 COLA was the smallest on record (just 0.3%). Altogether, there have been 11 years with a 2% or lower COLA since 2000.

But over the last three years, beneficiaries have enjoyed a hearty boost to their Social Security check. Cost-of-living adjustments totaling 5.9%, 8.7%, and 3.2% were passed along in 2022, 2023, and 2024, respectively. The 8.7% COLA in 2023 was the highest in 41 years.

If TSCL’s forecast proves accurate and Social Security recipients receive an estimated 2.6% cost-of-living adjustment in 2025, it’ll mark the first time since 1997 that there have been four consecutive years of COLAs totaling at least 2.6% (every COLA between 1988 and 1997 ranged between 2.6% and 5.4%).

What would a 2.6% COLA mean in dollar terms? For the average retired worker, their monthly check would increase by roughly $50. Meanwhile, the average worker with disabilities and average survivor beneficiary could expect their monthly payout to rise by $40 and $39, respectively.

Bigger COLAs simply aren’t cutting it for retirees

While the first four-year stretch of COLAs totaling at least 2.6% in 28 years would likely be cheered by those receiving a Social Security check, the fact remains that seniors continue to get the short end of the stick when examined over multiple decades.

In May 2023, TSCL released a study that compared aggregate Social Security COLAs between January 2000 and February 2023 to the price differences in a basket of goods and services regularly purchased by seniors. Whereas the aggregate COLA had increased by 78% since the 21st century began, the commonly purchased basket of goods and services had collectively risen in price by 141.4% since January 2000.

Put another way, the purchasing power of a Social Security dollar has plummeted by 36% since this century began. Even though COLAs have been a bit higher in recent years, they’re often still not keeping up with the actual inflation seniors are contending with.

The culprit behind this consistent loss of purchasing power is the CPI-W. As its full names suggests, it tracks the spending habits of “urban wage earners and clerical workers.” These are primarily working-age Americans who aren’t currently receiving a Social Security benefit. More importantly, they spend their money differently than the 86% of Social Security beneficiaries who are 62 or older.

For example, senior citizens spend a higher percentage of their monthly budget on shelter and medical care service expenses than the average American. On a TTM basis, shelter and medical care service inflation stood at 5.4% and 3.1%, respectively, as of May 2024, per the Consumer Price Index for All Urban Consumers (CPI-U).

Shelter inflation has remained stubbornly high due to the Federal Reserve’s hawkish monetary policy and rapidly rising mortgage rates. Meanwhile, medical care services inflation has picked up over the last seven months. The purchasing power of Social Security income continues to decline over time because the CPI-W doesn’t properly weight the costs that matter most to seniors.

I’m sorry to say that a forecast 2.6% cost-of-living adjustment in 2025 is unlikely to reverse this dynamic.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” ›

The Motley Fool has a disclosure policy.

Social Security’s 2025 Cost-of-Living Adjustment (COLA) Is on Track to Do Something That Hasn’t Happened in 28 Years was originally published by The Motley Fool

Source Agencies