MercadoLibre (NASDAQ: MELI) may not be a household name where you live. But that’s probably only because you don’t live where it operates. If you were a resident of South America, you most definitely would have heard of it. There’s even a good chance you’d be a customer. After all, it’s often referred to as the Amazon (NASDAQ: AMZN) of Latin America specifically because it’s got such a ubiquitous, Amazon-like presence there.

Just because you’re not a resident of its geographical market, however, doesn’t mean you can’t tap into growth potential. Indeed, investors outside of South America may want to make a point of plugging into this growth stock if only to add some regional diversification to their portfolio. Of course, it doesn’t hurt that MercadoLibre shares are also bringing some Amazon-like potential of their own to the table.

Being the Amazon of Latin America at the exact right time

The comparison to Amazon is a fair one, although it’s arguably incomplete. MercadoLibre is also a payment middleman and an e-commerce/online auction platform. It’s just as accurate to say that the company is akin to both PayPal (NASDAQ: PYPL) and eBay (NASDAQ: EBAY).

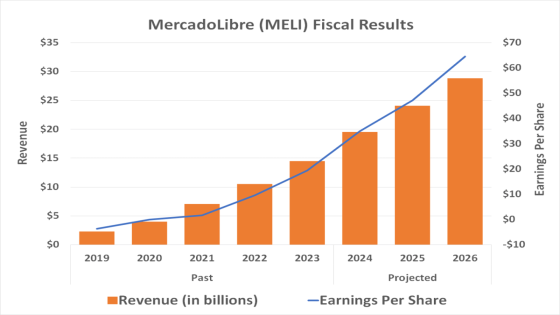

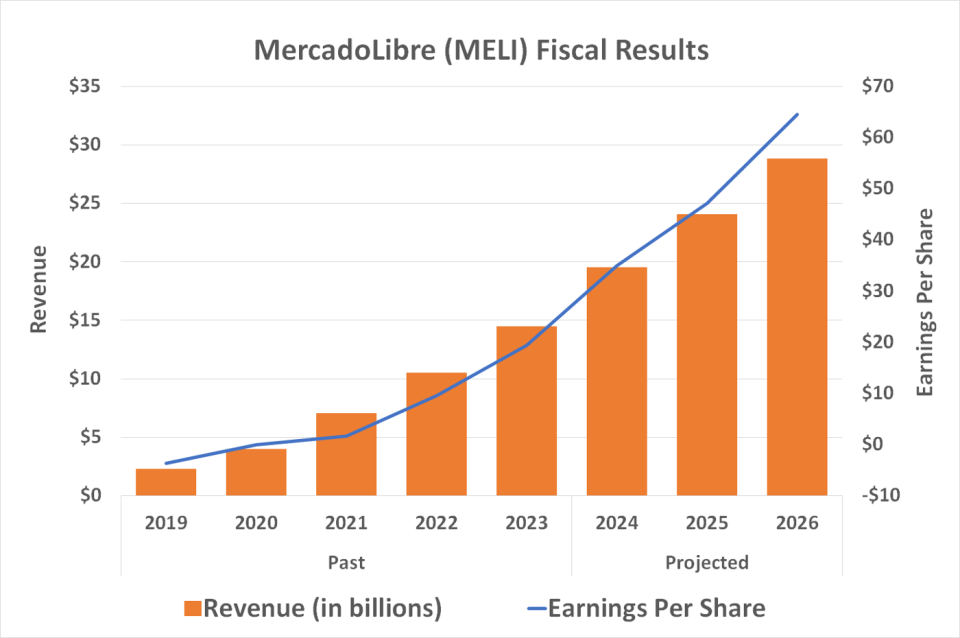

Whatever it is, it works. MercadoLibre’s first-quarter revenue was up 36% year over year, extending a long streak of similar growth. Last fiscal year’s sales of $4.2 billion were more than 40% better than the prior year’s top line.

What gives? How is this company growing so well in such a challenging economic environment?

In many ways (although not every way), Latin America is where North America was a couple of decades ago.

The rapid proliferation of internet-enabled smartphones underway right now is one of these ways. Numbers from market research outfit Canalys indicate shipments of smartphones to the region soared 26% to 34.9 million during the first quarter, marking the third consecutive quarter of double-digit growth after a prolonged, pandemic-prompted lull.

And yet, there’s plenty more room for continued growth of the continent’s number of smartphone users. GSMA suggests only 72% of Latin America’s residents own a mobile phone, while only 65% of this population uses a mobile internet service. More are on the way, though. GSMA believes the mobile internet’s penetration rate in South America will swell to 72% by 2030 when over half of these connections will be super-high-speed 5G connections.

As was the case in other parts of the world, online shopping is following the advent of widening access to the web. Market research outfit Americas Market Intelligence says Latin America’s e-commerce industry is set to grow to 24% this year, and expand another 21% next year and another 21% the year after that.

Why MercadoLibre is crushing it

MercadoLibre isn’t the only way to tap into this growth. It is, however, arguably the best way.

The company doesn’t operate everywhere in South America, but it’s doing business in 18 countries as well as Mexico. Notably, it offers its services in highly populated Latin American countries including Argentina, Colombia, and Brazil. While its market share varies widely from one country to the next, the company boasts more regular users of its services in the region than any of its rivals.

How has MercadoLibre done so well in such a highly fragmented and highly competitive economic environment? By pulling off the seemingly impossible task of (proverbially) being all things to all people.

Yes, it’s comparable to eBay. Just keep in mind that eBay isn’t solely an auction site. Plenty of sellers are operating online stores using eBay’s “buy it now” option, as they can with MercadoLibre. The company also facilitates stand-alone shopping carts for sellers looking to manage their own e-commerce website. MercadoLibre even offers logistics services, handling 90% of the parcels ordered through its platforms.

Bolstering the reach and penetration of the company’s e-commerce arm is its surprisingly robust suite of fintech solutions. See, MercadoLibre isn’t just a payment middleman. It facilitates loans, offers its own credit card, and supplies brick-and-mortar merchants with payment-acceptance equipment.

Combine all of these different components into a single, integrated operation. The whole is greater than the sum of the parts. MercadoLibre is a powerful ecosystem that’s not only in the right place at the right time but capable of keeping any and all of its competitors in check — including Amazon.

Don’t overthink it with MercadoLibre

Analysts seem to think it’s a winner. Their current consensus price target for MercadoLibre shares stands at $2,027.22, which is nearly 30% above the stock’s present price thanks to its recent lull. Of the 22 analysts covering the company, 17 of them rate it a strong buy, and none of these professionals consider the stock anything worse than a hold. The analyst crowd is also calling for an extension of its recent revenue and earnings growth, at least for the next several years, driven by the maturation of South America’s mobile tech industry.

With or without the analyst community’s bullishness, however, MercadoLibre’s story alone makes MercadoLibre stock a compelling growth prospect.

Bottom line: Don’t overthink it. If you’ve got a few thousand bucks you’re looking to put to work but aren’t finding anything you like well enough (that is to say, anything affordable enough) among the market’s usual growth suspects like Nvidia or Amazon, MercadoLibre is a great option most other investors aren’t even aware of. Their lack of awareness only bolsters the depth of your opportunity.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $20,960!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $39,620!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $366,195!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of June 11, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, MercadoLibre, Nvidia, and PayPal. The Motley Fool recommends eBay and recommends the following options: short July 2024 $52.50 calls on eBay and short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

The Ultimate Growth Stock to Buy With $3,000 Right Now was originally published by The Motley Fool

Source Agencies