Looking at the stock markets, three main points are commanding investor attention right now. First, and the most obvious, is that the stock indexes are near record-high levels. Both the S&P 500 and the NASDAQ are within touching distances of their all-time highs. Second, corporate earnings are sound, with most sectors showing double-digit year-over-year gains in the latest round of financial releases. And finally, while the Fed held steady on rates at its last policy meeting, there are signs that the pace of inflation is moderating, boosting sentiment for risk assets.

The Fed’s steady hand is a key point, in the eyes of John Stoltzfus, chief investment strategist at Oppenheimer. Stoltzfus sees a positive in recession avoidance, with further strength likely going forward. As he writes in his recent market strategy note, “In our view the good news for US investors in terms of the Fed is that it has been remarkably sensitive in applying its mandate to curb inflation this rate hike cycle and so far been able to avoid pushing the economy into a recession. The economy, business, the consumer and job growth persist in showing signs of resilience in data and earnings results…”

Some of the stock analysts at Oppenheimer are running with the upbeat outlook, staying bullish and suggesting two stocks to buy while markets are standing at record highs. We ran these tickers through the TipRanks database to see what other Street experts make of their prospects.

Landsea Homes (LSEA)

The first stock we’ll look at today is Landsea Homes, a Dallas, Texas-based homebuilder known for designing and building both homes and communities in desirable markets across the country. Landsea aims to provide best-in-class living areas, and has won awards for creating modern living areas in the suburbs and the cities, with single-family attached and detached homes, mid- and high-rise apartment properties, and master-planned communities. The company operates in high-end markets in New York and New Jersey, Arizona, Colorado, Florida, its home state of Texas, and in prime California locales such as Silicon Valley and Orange County.

While homes are big business, they are no business at all if they don’t get sold – and Landsea has its hands in the sales pot, too. The company provides financial and mortgage services in addition to building houses, with solid customer service and end-to-end support for homebuyers. Landsea’s financial side includes mortgage, home insurance, and title agencies, all under the Landsea name.

These combined businesses brought in $1.2 billion in total revenues last year, and the company followed that up with a solid top-line display to start 2024. In 1Q24, Landsea brought in revenues of $294 million, growing more than 21% year-over-year and beating the estimates by over $19 million. This result was driven by a total of 505 home closings in the quarter, with an average home price of $579,000. New home orders in Q1 came to 612, up 23% year-over-year.

At the bottom line, the company’s earnings came to 6 cents per share, by non-GAAP measures. While profitable, this missed the forecast by 7 cents per share.

Despite the earnings miss, the strong growth in home orders and revenue informed analyst Tyler Batory’s view of Landsea. In his coverage for Oppenheimer, Batory writes, “We see substantial growth potential the next few years driven by organic expansion and integration of several acquisitions. Volume growth should outpace G&A and expense inflation, contributing to a lower SG&A percentage and higher profit margins. The leverage profile should improve as well, as the company likely continues to execute on a balanced capital allocation strategy. These factors should contribute to multiple expansion, in our view.”

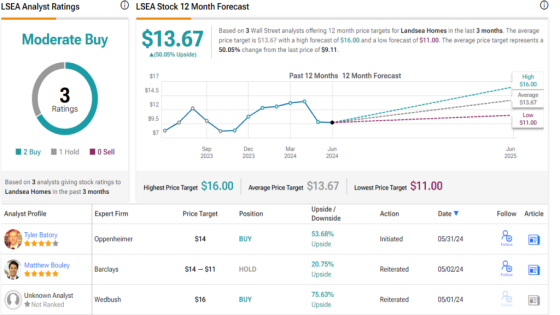

Looking ahead, Batory gives these shares an Outperform (Buy) rating, with a $14 price target that suggests a 12-month gain of 54%. (To watch Batory’s track record, click here)

Landsea’s Moderate Buy consensus rating is supported by 3 recent analyst reviews, including 2 Buys and 1 Hold. The stock is selling for $9.11, and its $13.67 average price target implies it will gain 50% in the coming year. (See LSEA stock forecast)

International Flavors & Fragrances (IFF)

Next up is a major name in the field of products and ingredients – a field that most of us don’t think about, but that impacts all of us. IFF is based in New York City and operates around the world, with offices and manufacturing facilities located in 44 countries. The company has its hands in a wide range of products, creating chemicals and products to enhance flavors and fragrances – the name of the company is simply descriptive – in categories as varied as nutrition, enzymes, soy proteins, and probiotics cultures. The company has end-use customers in the food, beverage, health and wellness, and pharmacy sectors. IFF is a member company of the S&P 500 index.

In recent months, IFF has been making moves to streamline its portfolio to create a more focused business. In March of this year, the company entered into an agreement with Roquette, the French ingredients company, for the sale of its Pharma Solutions unit. Roquette will acquire the unit for an enterprise value, estimated at $2.85 billion. The transaction is expected to close in 1H25. This was followed in April by IFF’s announcement that it had completed the sale of its Cosmetics Ingredients business to Clariant. The sale, which was announced in October of last year, included a purchase price of $810 million.

In the most recently reported quarter, 1Q24, the company showed a top line of $2.9 billion. While down 4.3% from the prior year, this revenue figure beat the forecast by $120 million. At the bottom line, IFF’s earnings came in at $1.13 cents per share, above the $0.86 Wall Street had in mind.

In addition, management stated that it expects 2024 revenue to hit the high end of the guidance range, which stands at $10.8 billion to $11.1 billion. This strength can be attributed to productivity gains; IFF saw approximately $185 million in productivity gains during 2023, and is on track to achieve $200 million in such gains for the current year.

This stock has caught the attention of Oppenheimer analyst Kristen Owen, who writes of IFF, “Amid its leadership and portfolio transformation, IFF is garnering a fresh look from investors. We see potential for a structural uplift in the IFF shareholder base as its portfolio rationalization focuses its commercial efforts in right-to-win categories, driving improved ROIC, and providing line-of-sight to a substantially healthier balance sheet. Thematically, IFF supports our thesis around molecules that matter as brand owners orient to a more health- and environmentally-conscious consumer.”

Owen goes on to conclude, “Now into what we would peg as the third inning of its transformation, the stock has seen a first leg up, and looks to have room to run with continued execution and balance sheet milestones.”

These comments back up Owen’s Outperform (Buy) rating on IFF shares. The analyst sets a $116 price target for the stock, showing her confidence in a 21% upside for the coming year. (To watch Owen’s track record, click here)

Overall, IFF gets a Moderate Buy consensus rating from the Street’s analysts, based on 15 recent reviews that break down to 6 Buys and 9 Holds. The stock has a current trading price of $95.98, and its $100.40 average target price implies a modest gain of 4.5% on the one-year time horizon. (See IFF stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source Agencies