Freelance marketplace Fiverr International (NYSE: FVRR) has fallen dramatically from its former glory as a darling of the early pandemic era. The stock is down 93% from the high it touched in February 2021, which has investors (understandably) doubting its merits as a long-term investment.

The company’s latest woes stem from the market’s concern that artificial intelligence (AI) could replace many of the jobs that freelancers offer to do on Fiverr, which would spell trouble for the marketplace’s long-term prospects.

But that fear appears misplaced to me, and this small-cap stock is far from down and out.

Pandemic skepticism is misplaced

Fiverr’s freelance platform connects buyers (procuring services) and sellers (providing services). It also adds value to each transaction in numerous ways, offering a convenient ecosystem for handling payments, correspondence, troubleshooting, etc. This creates a pleasant user experience for both parties. In exchange, Fiverr takes a slice of each transaction.

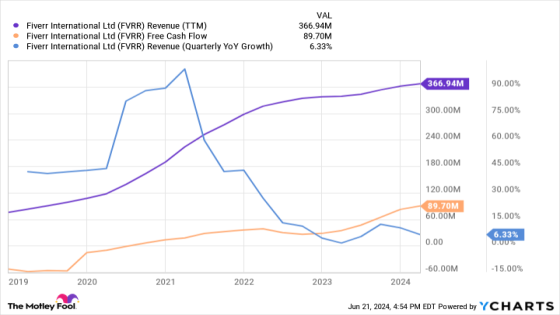

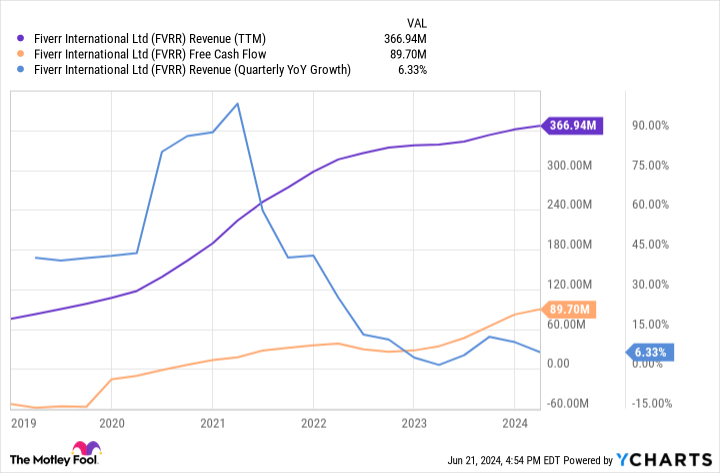

Both demand and supply for freelancing surged during COVID-19 when lockdowns and social distancing efforts shuttered many offices. That resulted in a growth spurt for Fiverr that pushed its revenue and the share price to great heights. However, its growth rate slowed to a crawl as the social distancing period receded, which triggered the stock’s decline.

Importantly, however, Fiverr didn’t give back revenue. Its growth slowed, but revenue never contracted.

It’s understandable that such up-and-down growth rates would spark skepticism about the stock. The good news is that Fiverr has accomplished some important things over the past several years. For starters, it turned free cash flow positive in 2020 and GAAP profitable a year ago. Additionally, the company has increased its take rate from 27.1% in Q1 2020 to 32.3% in Q1 2024.

That rising take rate signals that its platform still brings value. You could almost look at it as “pricing power.” Fiverr couldn’t continually increase its take rate if buyers and sellers didn’t see it as a worthwhile option; otherwise, they would leave. This bodes well for the company’s future.

Why AI is good for Fiverr

Artificial intelligence has emerged as the latest risk to Fiverr’s business model. The worry is that the buyers of services will start to use AI systems for more of those tasks, reducing the number of jobs offered on the platform, which would lead to an exodus among services sellers as well. That argument has some merit. Generative AI can quickly write copy, analyze documents, or create images. On the other hand, the rise of AI systems can also create new opportunities.

Management touched on this in the company’s Q1 earnings call, noting that AI has been a net positive for the platform because it’s creating growth in more complex tasks that are more profitable for Fiverr and harder to replicate elsewhere. Demand for AI-related services grew by 95% year over year in Q1. Fiverr stated that on its platform, there are 10,000 AI experts offering their services to help clients implement AI technology in their businesses. Also, spending-per-buyer grew by 8% year over year in Q1, indicating continued momentum in going “upstream.” (That’s jargon for larger buyers that pay more for services.)

Zooming out, Fiverr’s ability to transition into being a facilitator for more complex work arguably reinforces the platform’s long-term durability because it’s increasingly becoming a go-to option for companies that want to outsource labor instead of hiring employees. Small businesses will likely remain a core client group for Fiverr, but it’s clear the company wants to capture more dollars from enterprise-level customers.

A low-risk bet with massive upside potential

Fiverr’s investment potential looks compelling for a couple of reasons. First, it could see renewed revenue growth as the pandemic-driven growth spurt moves further into the past. Analysts estimate Fiverr’s revenue will increase by a mid-single-digit percentage this year. However, analysts also believe revenue growth will accelerate to 10% next year and 15% in 2026. Given that the company is now profitable, those upticks in top-line growth should produce similar jolts in earnings.

Meanwhile, Fiverr stock trades at a forward P/E ratio of under 10 today. That valuation is appropriate for a dying company, not one that just turned profitable and could see revenue growth accelerate in the coming years. Such a low valuation makes it more likely that Fiverr’s growth will trickle out to shareholders as share price gains. There isn’t much room for the stock’s valuation to go lower.

Remember that this is all based on estimates — only time will tell how matters actually shake out. But given the company’s strong financials and management’s comments on how AI is benefiting it, it’s hard not to like the setup for Fiverr stock here.

Should you invest $1,000 in Fiverr International right now?

Before you buy stock in Fiverr International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Fiverr International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $723,729!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Justin Pope has positions in Fiverr International. The Motley Fool has positions in and recommends Fiverr International. The Motley Fool has a disclosure policy.

This Small-Cap Stock Could Ride the AI Tailwinds to Market-Beating Returns. Time to Buy? was originally published by The Motley Fool

Source Agencies