Amazon Web Services leads the cloud market. Now Amazon (AMZN) wants to own the chips that power its cloud and boost profits by gaining share in the chips market, currently led by Nvidia (NVDA). Yahoo Finance got an exclusive first look at AWS’s latest chip, called the Graviton4. What makes this latest chip special? It’s the most powerful and efficient AWS chip to date. It’s 35% faster than the prior generation and has 75% more memory bandwidth. It’s the latest example of the research and development tech firms are willing to pour into chip development. AI is fueling demand for semiconductors – the guts that power the AI boom – meaning companies have to build those guts at a record-breaking pace. Whoever does it the fastest stands to grab up chip juggernaut Nvidia’s market share – currently 80% of the GPU chips market. That’s fueling a race between tech and chips companies, not only fueled by competition but also propelled by government incentives designed to fight back against China and have the United States retake the lead as the world’s dominant global chip manufacturer. Can AWS get a larger slice of the chips market pie? Here’s what’s next in the chips race.

If you’re going to future-proof your portfolio, you need to know what’s NEXT in the business of neurotechnology. In this series, Yahoo Finance will feature stories that give a glimpse at the future, and show how companies are making big moves today that will matter tomorrow.

For more on our NEXT series, click here, and tune in to Yahoo Finance Live for more expert insight and the latest market action, Monday through Friday.

Video Transcript

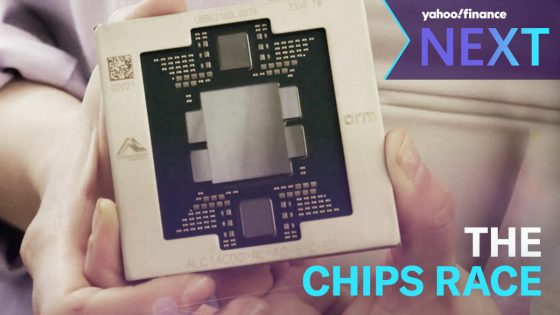

What I’m holding up here is our fourth generation Graviton processor that will be launching soon globally.

This is the brand new Graviton four chip from Amazon, its most powerful and efficient one yet the company exclusively shares with Yahoo Finance.

We will have launched four generations of Graviton delivering four x improvement in performance over that time period.

Amazon web services is currently the industry leader for cloud services, owning nearly a third of the total market with Microsoft’s Azure coming in at 25%.

Now, Aws wants to protect and boost its profits in two ways.

One by designing chips that can power its own cloud and two by positioning itself to capitalize off A I demand, but Aws is far from the front of the pack and they’re OK with that.

Aws says they’re not looking to overtake NVIDIA that could allow them to take a profitable slice of the massive and rapidly expanding A I driven chip market.

This is what’s next in the chips race to understand Amazon’s new chip.

It’s helpful to understand what chips do chips are in almost any device that has an on off switch, whether it’s a dishwasher or a car or the most sophisticated A I system.

Aws offers two main types of chips, those that power A I and general purpose chips, which is where chip like Graviton four comes in.

Some are focused on doing database, some are doing uh focused on doing web, some are focused on doing A I and Amazon not only buys chips from the people you would expect like A MD and Intel nvidia, but they actually design their own chips in house.

That’s Patrick Moorhead, a former A MD executive.

Now as a CEO and analyst, he has exclusive access to Amazon’s chips lab.

Among the most important factors for new chips, power and efficiency.

We get about three X amount of compute and three X amount of memory, about 75% more memory bandwidth and this will deliver about 30% better performance versus Graviton three and then further targeted workloads that now can benefit from the larger memory footprint.

We can receive up to 48 40% of higher performance improvement to do something like in memory analytics or databases.

That’s where this product will shine a lot more.

We need a lot of system memory available for you on the host node.

It’s not just about performance, it’s also about the bang for your buck.

Aw.

Customers can use Graviton four to cut their bill for it.

And in most cases with the same performance or higher performance at the same cost, Aws would not disclose details about Graviton four pricing but says processors are rented out at $0.02845 per second of compute power A W SS says in house testing speeds up chip delivery by eliminating the need to ship chips out for debugging.

It’s an evolution getting the first silicon out to actually making it production ready.

And it starts right here with looking at the silicon and sort of seeing how functional, how performant, how power efficient that process starts in Aws Debug lab at the automated test equipment station.

When we first got a Graviton four chip out of the manufacturing line, we install it in this machine here, we are looking for manufacturing defects and that gives us some early insight into the health of the silicon.

From here.

Engineers place each chip on a board there, it undergoes several tests that assess signal integrity and find any issues.

Lastly, the boards are placed in servers where Aws uses them to power things like their own large language models.

We basically take fully installed servers and racks and do more high level testing to make sure that we build them at the similar sort of logical concept that we would deploy them in our data centers.

Chips are a staggering part of the global economy because they’re needed to run practically everything we use.

This was acutely evident in the wake of the pandemic global supply chain disruptions caused massive backlogs in chip production.

And shipments.

The chips industry is currently valued at $544 billion and it’s expected to be worth more than a trillion dollars in less than a decade.

According to president’s research, that trillion dollar estimate driven by one thing demand.

There are two major sources for chips, chip makers and hyper scalar companies like Apple, Google, Microsoft and Amazon.

They’re developing chips to meet their specific needs to cut back on costs and offer customers more affordable alternatives.

All of these companies are spending a lot of money on developing chips.

Uh They won’t talk about how much they’re investing, but what they do have is they have these giant R and D budgets and let’s say you can save $200 a chip and you’re buying a million of them a year that adds up and that’s a lot of money that you can pour in to do that development is expensive.

Aw S would not disclose its overall chip spend.

I’m not convinced yet that it is a net money winner.

NVIDIA is currently viewed as the dominant chips player with a market capitalization to prove it, but there’s enough demand to go around.

According to analysts and executives, all of America’s biggest tech firms depend really fundamentally on chips that today are primarily or in a lot of cases exclusively manufactured in Taiwan by the S MC.

The Biden administration passed the Chips and Science Act in 2022 to bolster domestic chip manufacturing, investing $53 billion into the sector simultaneously.

A I is driving demand for chips.

That’s because I algorithms require complex computations and workloads which powerful chips can handle.

That’s where Aws hopes to find their lane.

Amazon does uh the design, they do the testing, they do the validation in house themselves as opposed to having an Intel and A MD or an NVIDIA do it and that allows them Aws to lower their cost and pass that on to their customers.

Aws has to make chips for their infrastructure.

A MD Intel and NVIDIA have to make chips for everybody’s infrastructure, right?

With every passing Graviton four, our goal is to make sure that it’s the cheapest option relative to other offerings, but then collectively it’s delivering more price performance, which means for every dollar spent you get a lot more performance, which is why customers really care more about price performance as a, as a value metric um that they focus on the new Graviton four chip is not an A I chip, but it’s an essential power mechanism behind the Aws chips that do power A I via and Ranum trainum competes directly with Nvidia’s A I chips.

The upcoming Blackwell ship from NVIDIA is expected to cost between $70,000.

According to Morehead, does Aws stand a chance against NVIDIA.

I like to call it coop.

NVIDIA needs Aws.

Aws needs NVIDIA.

Nvidia’s chips are the fastest and most powerful in the market driving the A I behind large language models like Chad G BT.

That performance is in part driven by NVIDIA prioritizing A I early for context on the timing, Amazon launched its cloud computing business in 2006.

The same year, NVIDIA released CAA programming language that can enable machine learning.

NVIDIA Bowls argue that A I was built off of the chip giants tech so it’s harder to transition to competitors.

Companies are willing to wait an entire quarter to get their chip orders in that timeline is according to U BS.

So where does this leave Amazon?

And its Graviton chip is the goal to get Nvidia’s customers to come over to aw not necessarily, there are different types of use cases that are better suited for different products.

If a customer is more focused on time to market NVIDIA based products that we offer and we offer the latest and the most diverse offerings and the largest scale of NVIDIA based products on the Aws cloud.

That is a great option.

So it’s not a zero sum game.

I think we will eventually find a spot for all different customers to operate regardless of what their choices for investors.

Earnings expectations from chip development may impact company profits more than the actual chips in production among Amazon Microsoft and alphabet analyst, earnings expectations are highest for Amazon, the profit margins just for Aws hit 38% in Q one of 2024 Aws has a lot of credibility uh in, in the semiconductor space.

And I mean, 10 years ago, I I had questions, right, how can a company like this?

Do chips when you have companies investing multiple billions of dollars to do that?

But it is very good.

That approach could fuel price reductions across the industry?

I do think it’s a risk mitigator to potentially get better pricing from Intel Ad.

And NVIDIA Aws hopes the Graviton four release alongside new servers that are four times as strong as current ones will position them as a formidable chips player in the competitive market.

It sounds like a big part of the competitive advantage you have is related to cost.

Absolutely.

And that’s what we can get with G and our train and influential product.

We can tune the product, tune the silicon to just focus on things that really matter for customer workloads.

That evolution could not only fuel future gains for aw it could potentially lead to more price diversification across an industry that continues to grow.

Source Agencies