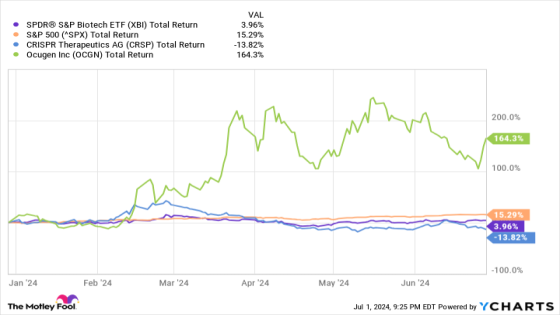

It hasn’t been a stellar year so far for biotech companies. The industry, as measured by the SPDR S&P Biotech ETF, is up just 4% since January, significantly lagging the S&P 500 ‘s nearly 17% gain.

Of course, it’s not hard to find stocks that have performed both better and worse than the sector average. Consider CRISPR Therapeutics (NASDAQ: CRSP), a mid-cap biotech that is down by 13% this year. On the other end of the spectrum is Ocugen (NASDAQ: OCGN), a small-cap drugmaker whose shares are up a stunning 164%.

That said, it’s not a good idea to rely on six months’ worth of data to decide which stocks to buy. These two biotechs will likely reverse positions over the long run, with CRISPR performing much better than Ocugen. Read on to find out why the former is worth investing in while the latter should be avoided.

XBI Total Return Level data by YCharts.

The stock to buy: CRISPR Therapeutics

Innovation is one of the keys to success in the biotech industry. CRISPR Therapeutics seems to have what it takes. It is an expert in the exciting field of gene editing.

Unlike many of its pure play gene-editing competitors, CRISPR already has an approved product on the market. The name is Casgevy, and it treats two rare blood diseases. It was developed in collaboration with Vertex Pharmaceuticals. Casgevy is the first approved gene-editing medicine that uses the CRISPR technique that earned its creators a Nobel prize.

Now, it’s too early to look at CRISPR Therapeutics’ financial results. Casgevy hasn’t been on the market very long, not to mention that administering this therapy takes a while. The biotech’s revenue in the first quarter was a measly $504,000, much less than the $100 million reported in the year-ago period. Its revenue comes from collaboration agreements with Vertex.

However, Casgevy’s opportunity is vast. CRISPR and Vertex estimate a potential population of at least 58,000 patients — 23,000 of whom are in Saudi Arabia and Bahrain. Those are important markets since the partners won’t have to battle Bluebird Bio — a biotech with competing gene-editing treatments — in these regions. At $2.2 million in the U.S., there is a multibillion-dollar opportunity here for CRISPR Therapeutics. The company will generate steady sales from Casgevy for a while.

In the meantime, CRISPR Therapeutics’ $2.1 billion in cash — a solid amount for a mid-cap biotech — will allow it to progress with its other exciting pipeline programs, some of which will produce excellent results in the future. Though CRISPR Therapeutics has produced market-beating returns since its 2016 initial public offering (IPO), it’s not too late to buy the stock.

The stock to avoid: Ocugen

Ocugen is a clinical-stage biotech that generates no profits. The company failed to make a dent in the COVID-19 vaccine market. However, it is making decent progress with its leading candidate, OCU400, a potential gene therapy for retinitis pigmentosa (RP), a group of rare eye diseases that cause blindness.

The company recently started a phase 3 study for OCU400. It also has several other programs in early-stage studies, including OCU410, a potential treatment for dry age-related macular degeneration, another eye disease. The biotech has even more assets in pre-clinical studies. Ocugen is doing what it is supposed to do as a clinical-stage biotech.

So why is it best to avoid the stock? First, virtually all biotechs at this stage are risky investments. Investing in a clinical-stage company that has produced outstanding phase 2 or 3 results in an extremely promising therapeutic area might be worth it. But that doesn’t apply to Ocugen.

Second, the company’s projections for OCU400 do not inspire confidence. Management believes it could earn approval in 2026 and go on to generate between $30 billion and $47 billion in the U.S. and the European Union. Ocugen also thinks OCU410 could rack up $75 billion in cumulative sales in the five years after approval.

Those estimates look optimistic. Excluding COVID-19 vaccines, it’s impossible to find therapies in the industry that generated sales of this magnitude that fast after approval. Ocugen’s claims should be taken with a cubic meter of salt.

Lastly, Ocugen doesn’t have a biotech giant in its corner as a partner to help it push these programs through the pipeline. While that’s not a requirement for success, it can be extremely helpful. And if Ocugen’s potential sales estimates were anywhere close to being on the mark, it would likely have a long line of potential partners racing to sign lucrative licensing deals.

Ocugen’s market capitalization is just under $440 million. Either the company’s estimates are on point — and not enough investors, analysts, and other biotech companies are seeing it — or the stock is as risky as the market seems to think. The latter is more likely, so it’s best for investors to stay away.

Should you invest $1,000 in CRISPR Therapeutics right now?

Before you buy stock in CRISPR Therapeutics, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CRISPR Therapeutics wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $826,672!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 8, 2024

Prosper Junior Bakiny has positions in Vertex Pharmaceuticals. The Motley Fool has positions in and recommends CRISPR Therapeutics, SPDR Series Trust-SPDR S&P Biotech ETF, and Vertex Pharmaceuticals. The Motley Fool recommends Bluebird Bio. The Motley Fool has a disclosure policy.

1 Biotech Stock to Buy Hand Over Fist and 1 to Avoid was originally published by The Motley Fool

Source Agencies