Taxpayers are holding their breath as Rachel Reeves prepares to unveil a £20bn black hole in the public finances.

The Chancellor is expected to announce the funding gap in a speech on Monday, blaming pressure on the NHS, prisons and schools.

It has fueled fears that a slew of tax rises in the Autumn Statement are on the way, as the Government attempts to balance the books.

Labour made a manifesto pledge not to raise National Insurance, income tax or VAT, but has refused to say which other taxes could be raised to provide funding for public services.

Ministers are thought to be considering changes to rules on pension savings, inheritance taxes and capital gains.

Pensions

Civil servants have already drawn up proposals for a flat 30pc rate of pension tax relief for the Chancellor’s review, The Telegraph understands.

It would mean that higher rate payers would be hit with an effective 10pc tax charge on their retirement contributions for the first time.

The plan would affect up to six million higher and additional rate taxpayers, costing the wealthiest savers around £2,600.

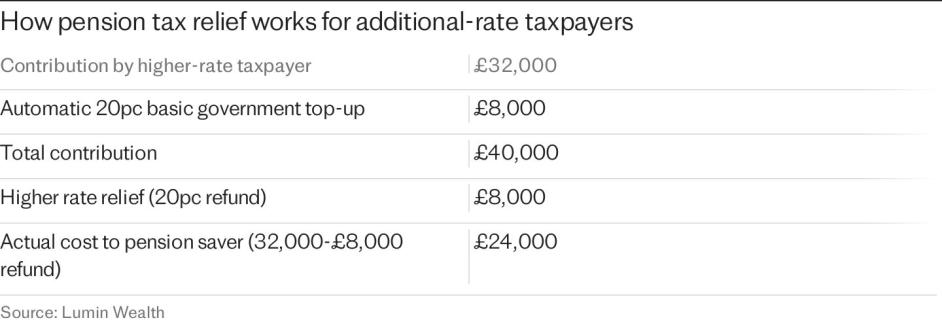

Pension contributions are tax deductible. This means that basic rate payers get a relief equal to 20pc of their payments to cancel out the income tax that would otherwise be due.

Higher rate payers – those earning more than £50,270 – get relief of 40pc, and most additional rate payers earning more than £125,140 get 45pc.

These rules cost the Exchequer more than £50bn each year.

A 30pc flat rate would raise the equivalent of a £2.7bn increase in tax, the Institute for Fiscal Studies (IFS) has said.

Ms Reeves has previously spoken in favour of restricting relief on pensions but has insisted she has “no plans” to change the current regime.

Labour may choose to target the tax-free lump sum instead, experts have warned. Currently, pensioners can withdraw 25pc of their pension pot without paying tax. This lump sum amount was frozen at a maximum of £268,275 under the Tories in 2020-21.

Capital gains

The Chancellor was also being lobbied by other Labour members in the run up to the election to align the rates of capital gains tax with those of income tax.

The Government’s own tax adviser the Office for Tax Simplification, a now-disbanded government agency, previously recommended the same tax rise, while the Liberal Democrats also advocate for the policy.

Capital gains tax is charged at 10pc or 18pc for basic rate taxpayers, and 20pc or 24pc for higher or additional rate earners.

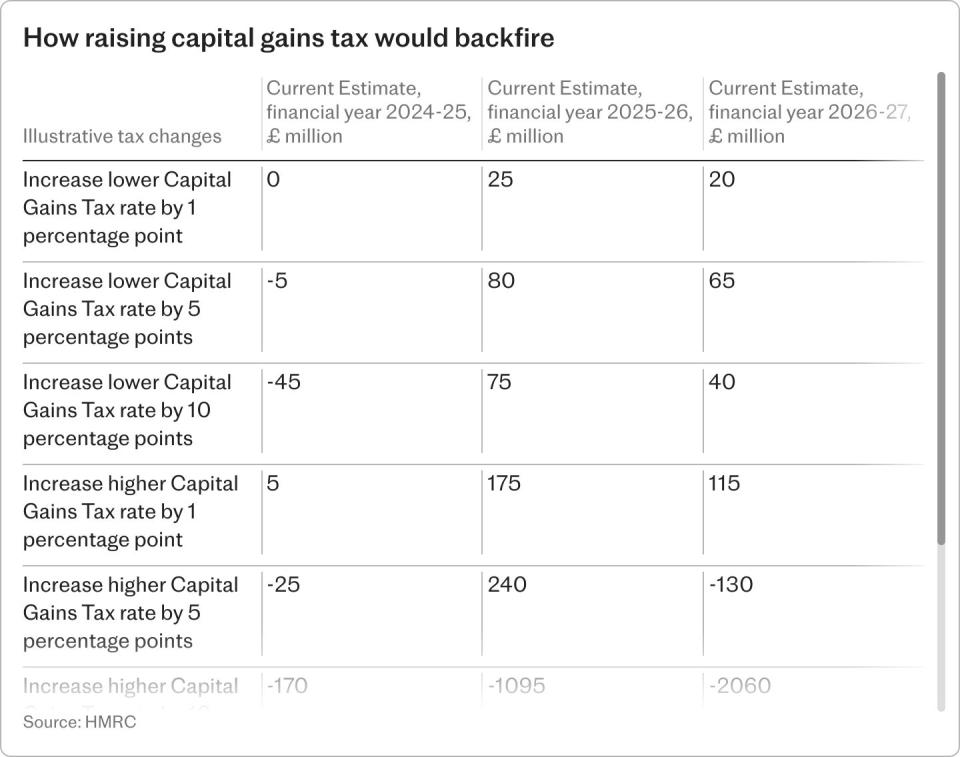

During the general election campaign, the Lib Dems claimed their plan to align the rates would raise £5.2bn. However, according to analysis by HM Revenue and Customs, raising the higher and lower rates by 10 percentage points would cost the exchequer just £3.5bn by 2027-28, as taxpayers would adapt their behaviour to avoid some of the rise.

Another option open to Labour is to start charging capital gains on assets passed on when people die – on top of inheritance tax, experts have said.

Currently, there is no capital gains tax due on death. Instead, any gains or losses accrued up to that date are effectively wiped out.

However, families do have to pay inheritance tax at 40pc on the value of an estate above the threshold of £325,000 – the “nil-rate band” – or £1m for a couple passing their home to their children.

Analysis by accountancy firm RSM has now shown that this double tax hit could result in effective tax rates for grieving families of over 50pc.

Investors have already suffered from changes to investment profit tax rules. The annual tax free allowance for capital gains tax was cut from £12,300 to just £3,000 under the previous government, making it much easier for investors to incur a liability.

Inheritance

Another option for Ms Reeves is inheritance tax. Chief Secretary to the Treasury Darren Jones told a public meeting in March that Labour could use inheritance tax to “redistribute wealth” and address “intergenerational inequality”.

At 40pc, Britain already has one of the highest death tax rates in the OECD.

The number of families paying the charge will hit nearly 44,000 a year by 2028-29, up from 33,000 this year, according to official forecasts. In total, almost 200,000 will pay the tax over the next five years.

But the number could be even higher if Labour chooses to increase the tax burden.

Currently, homeowners can pass on £500,000 – or £1m if they are a couple – as long as they leave their house to their children. Labour could choose to cut or lower this exemption, widening the scope of inheritance tax.

The Chancellor has also been urged to abolish inheritance tax relief for shares in fast-growing companies in order to raise an estimated £1.6bn a year for the Treasury.

Scrapping business relief on inheritance tax would raise £1.4bn, while increasing the standard rate from 40pc to 41pc would raise a total of £460m by 2027-28, according to HMRC analysis.

There is also a risk that Labour extends the scope of inheritance tax to cover pension pots, which are currently protected, experts have warned.

Under current rules, if someone dies before the age of 75, any of their unused pension is inherited tax free. For anyone who dies after this age, income tax applies at the point the beneficiary withdraws the money.

Analysis shows that families inheriting a £100,000 pension – roughly the size of the average pension pot for a 55 to 64 year old – could be stung with a £65,000 tax bill if tax were applied on death.

Source Agencies