We have entered a new age of nicotine consumption. Led by Philip Morris International (NYSE: PM), consumers around the globe are turning from traditional cigarettes to safer ways to maintain their nicotine habits. The global tobacco giant is smartly cannibalizing its existing cash cow to position itself to dominate new markets in the coming decades.

Reporting second-quarter earnings on July 23, Philip Morris showed strong growth yet again. Even though the stock is up close to 20% year to date, it still has a healthy dividend yield of 4.6% compared to the S&P 500‘s yield of 1.3%. Does that make this dividend growth stock a buy?

Stable volume and growing tobacco profits

Philip Morris International owns the Marlboro brand for every geography outside of the U.S. and China, as well as some other long-standing cigarette brands. Unlike in the U.S. where cigarette volumes are collapsing, the business has remained relatively stable in international markets due to population growth and greater cultural acceptance around smoking.

Through the first half of 2024, Philip Morris’s cigarette shipments were flat year over year, but thanks to price increases, combustibles net revenue grew 4.3% year over year. And after nearly two years of shrinking profitability for this segment, management expects combustibles gross margin to improve in the second half of 2024, adding to its 50 basis point expansion last quarter.

Despite foreign exchange headwinds, exiting the Russian business, and declining usage in some markets, Philip Morris International’s cigarette business has remained stable for many years now.

Cigarette profits drove the bulk of Philip Morris’s more than $10 billion in trailing operating income, and investors should have confidence they will be around for years to come. But this isn’t all Philip Morris has up its sleeve.

Can new products drive further growth this decade?

Through years of research and major acquisitions, Philip Morris has not only become the global leader in cigarettes but also the leader in new-age nicotine products. Smoke-free products such as Zyn nicotine pouches or heat-not-burn iQOS devices now make up 38% of company revenue, up from close to zero 10 to 15 years ago.

This incredible growth in such a short time span has made Philip Morris a much more durable and diversified business, reducing the risk posed by long-term cigarette usage declines. Philip Morris now has 36.5 million smoke-free product customers and is adding millions of new customers around the globe every year. In the first half of 2024, smoke-free revenue grew 21% year over year and is becoming a larger part of the business every quarter.

With plenty of room to grow in new markets (iQOS has yet to launch in the U.S. as just one example), smoke-free products can fuel revenue growth at Philip Morris for years to come and make this stodgy tobacco name a growth stock hiding in plain sight.

Consistent dividend growth will continue

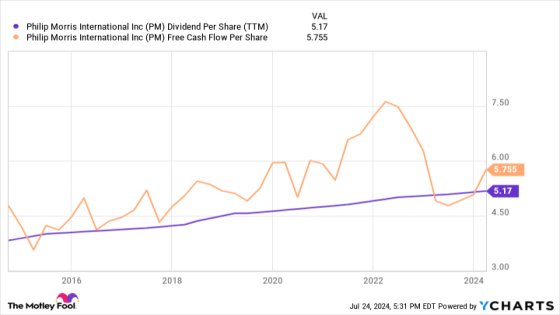

If you look at Philip Morris’s trailing numbers, you might think it’s only barely able to pay its dividend yield of 4.6%. It has a dividend per share of $5.17, covered by free cash flow per share of $5.76. Its dividend payout ratio is quite high on a trailing basis, which may further lead investors to believe the company is walking a fine line to maintain the current payout.

But Philip Morris has depressed profit margins right now. Due to heavy investments in its smoke-free offerings, the company’s operating margin has fallen to 34%, down from 40% a few years ago. Not only can Philip Morris’s revenue grow going forward, but its profitability should also improve thanks to the increased contribution of smoke-free products. Organic gross margin for this category was up 220 basis points in the second quarter. If these trends hold, free cash flow per share should inflect higher as well.

Add it all up, and Philip Morris International looks poised to sustain its payout growth long term. Buy this high-yield dividend stock, sit back, and let it fuel steady returns for your portfolio.

Should you invest $1,000 in Philip Morris International right now?

Before you buy stock in Philip Morris International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Philip Morris International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends Philip Morris International. The Motley Fool has a disclosure policy.

Philip Morris International: Time to Buy the Ultimate Dividend Growth Stock? was originally published by The Motley Fool

Source Agencies