Are you looking for a new income-producing pick? They’re out there, to be sure. But, given that interest rates are still near multi-year highs, yields on most dividend stocks seem strangely low. You might want to look a bit off the beaten path if that’s the kind of holding you’re interesting in adding to your portfolio.

Income-minded investors should consider taking on a new stake in a company called Vici Properties (NYSE: VICI) sooner rather than later. It’s far more resilient than it seems like it should be on the surface.

What’s Vici Properties?

Never heard of it? Don’t sweat it. Most investors probably haven’t. While its $33 billion market capitalization is by no means small, it’s nowhere near the size of the technology giants that dominate the headlines these days.

It’s a real estate investment trust (or REIT), first and foremost. These are organizations that own rental real estate, passing along the majority of their rent-driven profits to shareholders in the form of dividends. REITs’ focus can range from hotels to office buildings to strip malls to apartments.

Even by REIT standards, however, Vici is relatively unique. Most of its revenue comes from the 54 properties that are currently home to a casino, and quite often a related hotel. Vici Properties doesn’t own the casinos located on its land, to be clear. Rather, it leases these sites to operator tenants like MGM Resorts and Caesars (although Vici and its tenants clearly have a common interest).

The company also owns a handful of non-gaming experiential sites, although these only account for a fraction of its total business.

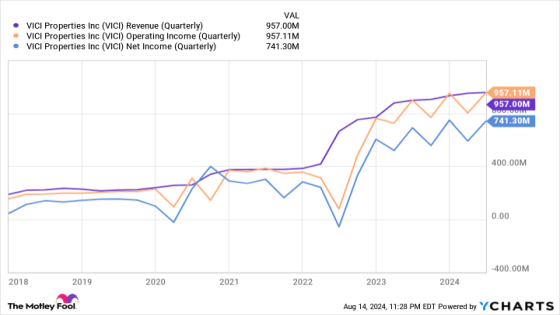

Wherever it comes from, it’s coming reliably, and increasingly so. Last quarter’s revenue reached $957 million, up 6.6% despite fresh economic headwinds. Per-share profits improved from $0.69 to $0.71, of which $0.415 was dished out to shareholders as a dividend. The quarter’s results and payout extend longstanding trends.

3 reasons to buy Vici stock

The REIT’s historical results are solid enough, but is Vici an above-average prospect that offers more than comparable alternatives? Yes, it is, for three reasons.

1. The gambling business is always growing

Vici’s top and bottom lines aren’t directly driven by the casinos operating on its properties. But there’s an obvious connection between the two. If their gambling business is strong, its tenants are better equipped to pay their rent. A strong casino industry also creates opportunities to buy and develop more properties in the future.

To this end, the U.S.’s casino gambling business continues performing surprisingly well despite recent economic turbulence. The American Gaming Association reports that the U.S.’s first-quarter gambling revenue reached a record-breaking $17.67 billion, up 26.1% year over year thanks to the strong growth of sports betting, and higher for a 13th consecutive month in March.

The second quarter’s results aren’t posted yet, but the industry’s handle was still growing well through May of this year. This persistent growth reflects the resiliency of the businesses behind so-called “vice stocks,” which generally perform well even when other industries are running into cyclical headwinds.

2. There are several compelling growth levers to pull

While the bulk of Vici Properties’ sales and profits are produced by its casino-related properties, the REIT understands that a sole focus on one industry is limiting and a bit risky. It also owns 39 experiential non-gambling properties plus four golf courses, diversifying its profit centers.

More such projects are on the way. It’s also facilitating a loan to Great Wolf Lodge to develop destination resorts on Vici land. Early this year, it made a loan to fund the development of a Margaritaville Resort in Kansas City, Kansas, which will be linked to a youth sports training facility and baseball center.

Backing such developments seems risky in a wobbly economic environment like the one we seem to be in. But things may not be quite as wobbly as they seem. The inflation that’s been nagging consumers for a couple of years now is finally abating, with last month’s consumer inflation rate falling to a multi-year low of under 3%.

Moreover, even before July’s inflation figures were released, Deloitte was touting that its U.S. Financial Well-Being Index for June reached a multi-year high. Intentions to spend on leisure travel were particularly strong, suggesting that Vici’s loans made to future tenants are actually sound investments.

3. Vici stock’s dividend yield is strong

Newcomers will be stepping into a REIT that’s yielding a solid 5.3%. That’s a yield based on a dividend, by the way, that’s grown every year since 2019, and will likely continue doing so.

Affordability is certainly no problem, either. Much like last quarter’s dividend and earnings, Vici’s dividend payments have historically only consumed about two-thirds of the REIT’s profits. The rest can be reinvested in the organization’s own growth.

In this vein, Vici Properties has never had any trouble raising money to fund new projects — the marketplace knows this company picks and plans its developments wisely. Of course, with shares priced at only a little over 12 times the company’s trailing earnings and less than 12 times its forward-looking profits, investors know they’re getting a bargain as well.

Not great for growth, but great for income

Vici Properties isn’t necessarily the right fit for everyone’s portfolio, to be clear. If you’re only looking for growth, while Vici offers it, it doesn’t offer enough of it to fulfill that role. Consider a different prospect.

If you’re looking for reliable dividends and respectable dividend growth but aren’t finding great yields with most of the familiar names, however, Vici Properties is for you. The fact that the stock’s not really moved much since making its 2021 high only makes it that much more attractive now. The market’s likely to start connecting all these dots soon enough.

Should you invest $1,000 in Vici Properties right now?

Before you buy stock in Vici Properties, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vici Properties wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $763,374!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Vici Properties. The Motley Fool has a disclosure policy.

3 Reasons to Buy Vici Stock Like There’s No Tomorrow was originally published by The Motley Fool

Source Agencies