“The true investor welcomes volatility. A wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses.” This quote from Berkshire Hathaway‘s legendary CEO Warren Buffett highlights the opportunities that can be created when stocks see substantial short-term valuation pullbacks.

Even with the broader market marching higher this year, there’s still plenty of opportunity for investors to capitalize on. With that in mind, read on to see why two Motley Fool contributors think buying these stocks while they’re still down big could help you score market-crushing returns.

This AI stock trades at a surprisingly low earnings multiple

Keith Noonan: Super Micro Computer (NASDAQ: SMCI) builds high-performance servers that are used in data centers. Using Nvidia‘s market-leading graphics processing units (GPUs) as key components, the company delivers powerful computing machines capable of running advanced artificial intelligence (AI) applications.

With demand for AI processing surging, Supermicro has seen its sales and earnings skyrocket. Revenue rose 110% to hit $14.9 billion in the company’s last fiscal year, which ended June 30. Meanwhile, non-GAAP (adjusted) earnings per share rose 87% to hit $22.09.

It looks like the strong growth is poised to continue. For the current fiscal year, Supermicro is guiding for sales to come in between $26 billion and $30 billion. If the company were to hit the midpoint of that guidance range, that would mean delivering annual sales growth of 87%.

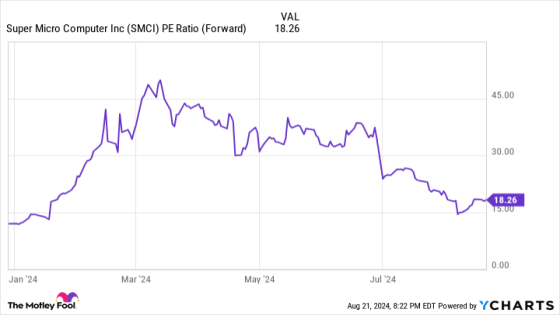

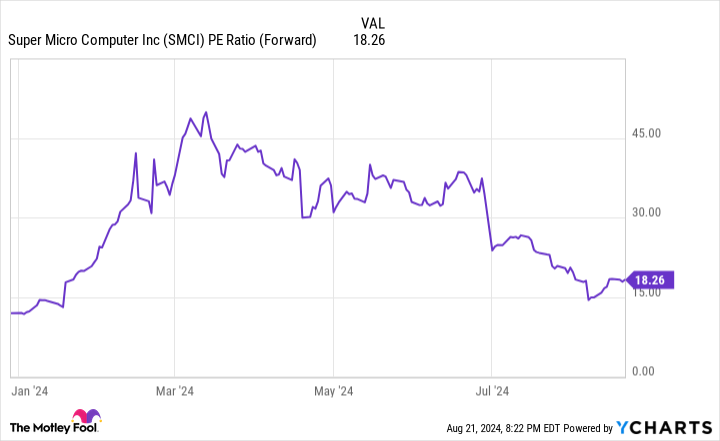

Despite the business’ incredible growth and impressive near-term performance outlook, the company is valued at just 18 times this year’s expected earnings on the heels of recent volatility. Supermicro’s share price is also still down 48% from the high that it reached in March. Why is the stock trading at such a steep discount compared to its growth rates?

For starters, the company saw some weakening on the margins front. Its gross margin came in at just 11.2% last quarter, down from 15.5% in the previous quarter and 17% in the fourth quarter of fiscal 2023. Investors are also concerned about the cyclicality of demand for AI processing hardware.

If demand for its high-end rack servers increases substantially again in Supermicro’s next fiscal year, the passage of time will likely show that the company’s stock was significantly undervalued at current prices. Some investors are betting that demand will level off or take a step back, but they may be underestimating demand for AI-tailored servers.

While many tech giants have already invested heavily to ramp up their processing capabilities, there’s no sign of letting off the gas yet. Spending among medium-sized players may also still be in much earlier stages of ramping, and demand from government customers looks poised to increase significantly over the next five years.

Charting demand cycles for AI hardware involves plenty of speculation, and Supermicro is undoubtedly a high-risk, high-reward stock. But with shares trading at levels that look low given the business’ growth rates and industry backdrop, the server specialist looks like a worthwhile buy.

ON Semiconductor’s strategic positioning makes sense

Lee Samaha: Electric vehicles (EVs), energy infrastructure (including renewables), advanced driver assistance systems (ADAS), EV charging, industrial automation, and 5G cloud are all great long-term markets, and that’s why ON Semiconductor‘s (NASDAQ: ON) management is positioning the company in them.

On the other hand, most of these end markets are under pressure in 2024. Relatively high interest rates continue to curtail auto sales (including EVs) and, in turn, EV and ADAS investment. In addition, the industrial automation market is going through a weak period due to weaker economic growth, distributors running down inventory, and slowing order growth.

That’s why CEO Hassane El-Khoury continues cautiously talking of an “L-shaped” recovery, rather than the V-shape beloved of contrarian investors.

His position is understandable. A recovery in auto sales and industrial investment won’t be immediate, as there’s often a delay in spending when interest rates are cut as consumers and businesses wait to see how much lower rates will go. In addition, ON Semiconductor’s revenue is its customers’ capital spending plans, and it takes time for projects to get approved, as automotive and industrial customers monitor their end markets.

There’s no denying that ON Semiconductor is well-positioned in strong end markets, and many long-term investors prefer not to speculate on market timing. Management shares that view and recently committed up to $2 billion in investment in a manufacturing facility to support future growth, not least from a deal to supply Volkswagen with silicon carbide chips.

Despite promising opportunities on the horizon, ON Semiconductor stock is trading down roughly 30% from its high. Moreover, at slightly less than 19 times the expected 2024 earnings, the stock looks an excellent value, whether the recovery is merely an initial “L” or not.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

Keith Noonan has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends ON Semiconductor. The Motley Fool has a disclosure policy.

2 Tech Stocks Down 48% and 30% to Buy Right Now was originally published by The Motley Fool

Source Agencies