SpaceX has been a remarkable success over the last 15 years. It brought the space flight industry in the United States — really, around the world — back to life and inspired plenty of copycats along the way. The age of commercial space flight is upon us and set to grow like gangbusters over the next 10 to 20 years. By 2050, the United Nations believes the space economy could be worth $3 trillion.

Industry experts believe that SpaceX has a de facto monopoly on commercial rocket launches right now, which is why its valuation has surpassed $200 billion. But that monopoly may be turning into a duopoly quickly. Enter Rocket Lab (NASDAQ: RKLB). Started by New Zealand entrepreneur Peter Beck, it is now the only other company, along with SpaceX, to reliably and safely perform rocket launches for commercial customers.

Rocket Lab is growing like gangbusters and recently hit a $3.5 billion market cap. But the party might just be getting started. I think Rocket Lab has a chance to be worth more than SpaceX in 10 years and be a home run for investors. Here’s why.

Rapid growth, minimal competition

Rocket Lab entered the rocket launch market with a small system it calls the Electron. It needed to attack SpaceX at the edges, providing a nimbler, smaller, and cheaper launch vehicle for customers looking for this niche. The product has built a ton of momentum in recent years. In fact, it recently hit 50 launches, making it the fastest commercially developed rocket to reach 50 launches in history. Growth is accelerating, too, with a 100% launch frequency increase from the second half of 2023 to the first half of 2024.

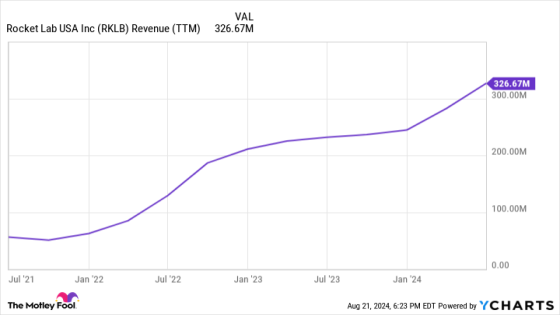

This momentum has led to a lot of recent customer wins. Year to date the company has signed 17 new Electron launches, increased its backlog to over $1 billion, and grew revenue 71% year over year last quarter. The business is humming in 2024.

Since SpaceX is focused on larger launches, it is unlikely to attack Rocket Lab’s position with small commercial launches. And, since no other rocket launch competitor has been able to consistently perform launches, Rocket Lab has a monopoly in the small launch market at the moment. Not a bad place to be.

Upscaling to larger launches

The Electron is not all Rocket Lab wants to be. It is currently working on the Neutron rocket (sense a pattern in naming them?), which will be much larger than the Electron and can carry around 40 times the payload for customers. Commercial launches are paid for by weight, meaning we could see a huge increase in revenue once the Neutron system gets fully operational.

Over the last 12 months, Rocket Lab has generated $327 million in revenue. Not all of this comes from the Electron launch segment (more on this later), but a good portion of it does. According to insiders, SpaceX has been able to charge $5,000 per kilogram or more on its Falcon9 rocket to customers.

If the Neutron can charge the same, it will generate $65 million in revenue per launch just from the payload payments, or 20% of its total revenue over the last 12 months. The good news is that the Neutron is slated to become open for commercial customers within the next few years.

Grand ambitions and a focused leader

Rocket Lab’s next leg of growth should come from the Neutron system. However, it has grander ambitions than just launching satellites into Earth orbit. The Neutron rocket will be capable of housing humans, meaning Rocket Lab could take astronauts to the Moon or even Mars. It already has contracts for unmanned Mars missions with NASA and other U.S. government agencies.

On top of rocket launches, Rocket Lab is working on building and selling space systems equipment to customers. These include things like space solar panels and space capsules for missions.

Over the long run, it hopes to build up a third leg to its business model with space data and services. As one of the only companies vertically integrated for space launches, it has extremely valuable data from orbit. This could be the most valuable part of Rocket Lab’s business model, as software and data services come with high profit margins.

Another positive for Rocket Lab is its focused leader. Elon Musk built SpaceX, but he owns and operates many other businesses including Tesla, Twitter, and Neuralink. It’s not a stretch to call him distracted. Rocket Lab’s visionary founder Peter Beck’s sole focus is on building this company, which I believe is an advantage as it tries to break into SpaceX’s monopoly.

It might not look like it today, but I think there is a good chance that Rocket Lab can take its $327 million in revenue and transform into a business generating tens of billions of dollars in revenue per year 10 years from now. Even if it takes longer than 10 years, Rocket Lab has a chance of taking its $3.5 billion market value and eventually surpassing SpaceX’s $200 billion valuation.

Spaceflight is far from a low-risk sector, but Rocket Lab looks like a promising growth stock with a ton of potential upside for investors right now.

Should you invest $1,000 in Rocket Lab USA right now?

Before you buy stock in Rocket Lab USA, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Rocket Lab USA wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends Rocket Lab USA. The Motley Fool has a disclosure policy.

Prediction: This Hypergrowth Space Stock Will Be Worth More Than SpaceX In 10 Years was originally published by The Motley Fool

Source Agencies