Enbridge (NYSE: ENB) is an $85 billion midstream giant with a business that spans across North America. Its dividend yield is 6.7%, which is multiples of the 1.2% yield you’d collect from the S&P 500 index and the 3.1% on offer from the average energy stock, using Energy Select Sector SPDR ETF (NYSEMKT: XLE) as an industry proxy.

The only problem is that Enbridge’s shares have rallied strongly over the past six months. Is this high-yield stock still worth buying?

What does Enbridge do?

From a very basic perspective, Enbridge is built from the ground up to be boring. The core of its business (around 75% of EBITDA, or earnings before interest, taxes, depreciation, and amortization) comprises oil and natural gas energy infrastructure, such as pipelines.

Energy companies pay Enbridge fees for the use of these vital transportation assets, which provides the company with very reliable cash flows. Demand for energy is far more important to the volume of its pipes than the price of the products being moved through the system.

The rest of the business is a mix of regulated natural gas utilities (22% of EBITDA) and renewable power. Regulated utilities are granted monopolies in their regions in exchange for giving the government oversight on rates and capital spending plans. Like pipelines, this business is, by regulatory decree, intended to be boring and reliable. Meanwhile, the company’s renewable power portfolio is contract-driven, so it, too, generates consistent cash flows.

There are two takeaways here. First, Enbridge’s business is purposefully spread from oil, a dirtier energy source, to solar and wind power, clean energy sources. A primary goal is to provide the world with the power it needs, which increasingly means shifting toward cleaner energy sources. That shift will continue.

Second, everything the company does is intended to create reliable cash flows. This is what has supported Enbridge’s 29-year streak of annual dividend increases and its lofty 6.7% dividend yield.

A good run for Enbridge

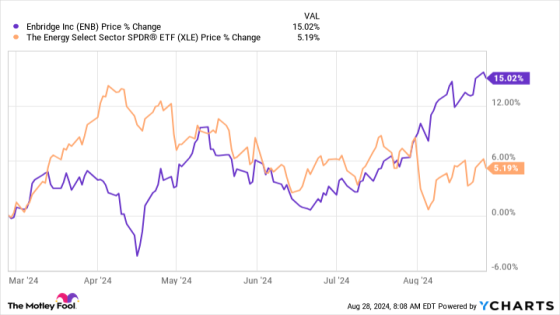

That dividend yield, however, was over 7% not too long ago. That’s because investors have pushed Enbridge’s shares sharply higher over the last six months, with the stock’s 15% or so gain easily besting the average energy stock’s 5% gain.

The expectation of falling interest rates is likely part of the reason for the gain, given that the midstream sector tends to make heavy use of leverage. Within the sector, Enbrige tends to use more leverage than its peers because of its exposure to regulated utility assets. Thus, lower rates are likely to be a particular benefit to Enbridge’s business.

But Enbridge has also been in the process of buying three regulated natural gas utilities from Dominion Energy (NYSE: D) over the past few months. It is just about done with the last of the three transactions, so the uncertainty around the funding of the deal is less of a concern than it was. Plus, the three utilities will solidify Enbridge’s growth plans with highly regulated investments. Such investments tend to take place regardless of the market environment.

All in all, the rise in price is probably a justifiable reflection of Enbridge’s improving outlook. But has the advance priced in all of the value here? Not if you are a long-term dividend investor. The big yield here will likely make up the lion’s share of your return, but that’s by design.

Augmenting that will be dividend growth, which should probably be in the low- to mid-single digits over time. But add around 3% (roughly keeping the dividend in line with inflation growth) to 6.6% and you get 9.6%, nearly the 10% return most expect from the broader market. Dividend growth above that figure only makes the story better.

Not as attractive, but still attractive

Enbridge isn’t as much of a bargain as it was just a few months ago. That’s just a simple fact, given the notable stock price increase. But it remains an attractive income stock just the same, thanks to the still-lofty yield, reliable cash flows, and improving fundamentals. That and the fact that the stock is still trading around 15% below its 2022 high-water mark. Indeed, there might even be some additional recovery potential here before the upturn has fully played out.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $720,542!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Reuben Gregg Brewer has positions in Dominion Energy and Enbridge. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

Is High-Yield Enbridge Stock Still a Buy? was originally published by The Motley Fool

Source Agencies