The e-commerce industry is jam-packed with competition.

Niche marketplaces such as Etsy and Wayfair have managed to fend off competition from larger industry stalwarts Amazon and Walmart. Moreover, platforms like MercadoLibre and PDD Holdings have proved to be formidable players overseas.

But there is one e-commerce marketplace stock that deserves consideration for your portfolio right now. Amidst this intense competition, the company can easily be overlooked despite being being an attractive choice for growth investors.

This stock just hit a 52-week high

It’s no secret the capital markets have been roaring for some time now. After a dismal performance in 2022, the S&P 500 and Nasdaq Composite rebounded sharply last year, and that momentum has largely extended into 2024 with both indexes posting gains of roughly 17% year to date.

However, over the last month or so, both the S&P 500 and Nasdaq Composite have experienced notable sell-offs. Considering September is historically one of the heaviest selling months in the stock market, more pronounced dips could very well be on the horizon.

And yet, despite these drops, my pick for an e-commerce stock has outperformed the broad market over the last month. The stock’s $64 price tag as of this writing represents a 52-week high.

The company is buying back shares

Sometimes, when a stock starts to kick into gear, it’s best to sit on the sidelines and let the price action sort itself out. One reason for this is that momentum traders may be playing a role behind the scenes, helping push the stock price higher despite what the fundamentals may suggest is appropriate. That’s unlikely to be the case here, though.

The company has been buying back shares in droves. In 2023, it repurchased $1.4 billion of stock. And through the first six months of 2024, it repurchased another $1.5 billion of stock. Those buybacks reduced the company’s outstanding share count nearly 10%.

One of the biggest reasons a company repurchases shares is because management sees the stock as undervalued, and I have to agree.

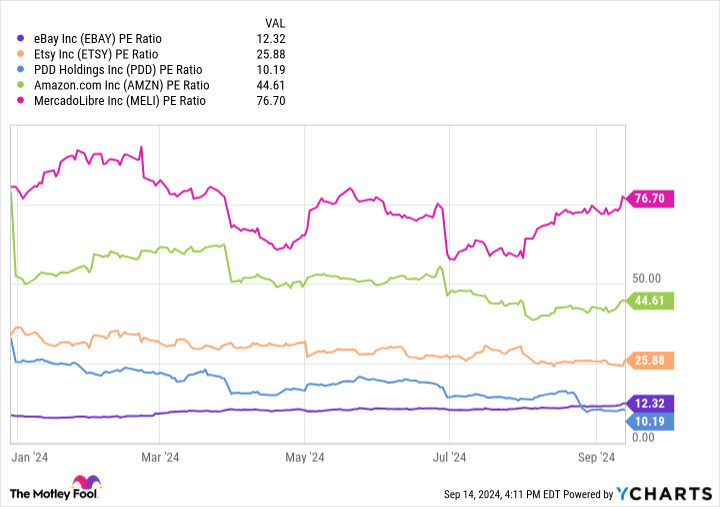

Its valuation is dirt cheap

The company in question is eBay (NASDAQ: EBAY). Back in late December, Fool.com contributor Parkev Tatevosian called for buying eBay stock “hand over fist” in 2024. Since that article was published, shares have climbed an impressive 46%.

But shares of eBay are still cheap. Right now, eBay’s price-to-earnings (P/E) ratio of 12.3 is among the lowest compared to other leading e-commerce stocks.

Moreover, the company’s forward P/E of 13.2 is drastically lower compared to the S&P 500’s forward P/E of 22.6. These disparities in valuation multiples could suggest that investors see eBay’s prospects as less enticing compared to its peers or the broader market.

How can a stock that’s trouncing the market this much be valued at such a steep discount to the competition?

Many of the top e-commerce stocks are larger, more diversified platforms like Amazon or MercadoLibre. That’s helpful when investors are somewhat skittish around the prospects for e-commerce more broadly. A cloudy macroeconomic environment has made assessing all sorts of investments quite difficult over the last couple of years, especially opportunities revolving around consumer discretionary spending.

However, inflation continues to cool down, and I wouldn’t be surprised if e-commerce stocks in general start to witness some newfound enthusiasm.

Overall, the combination of ongoing share buybacks, a steep discount to its peers, and the long-term growth in online shopping make eBay stock a no-brainer buy right now — and especially so during the next market downturn.

Should you invest $1,000 in eBay right now?

Before you buy stock in eBay, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and eBay wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $729,857!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon. The Motley Fool has positions in and recommends Amazon, Etsy, MercadoLibre, and Walmart. The Motley Fool recommends Wayfair and eBay. The Motley Fool has a disclosure policy.

If I Could Only Buy 1 E-Commerce Stock During the Next Market Sell-Off, This Would Be It (Hint: It’s Not Amazon) was originally published by The Motley Fool

Source Agencies