Carnival (NYSE: CCL)(NYSE: CUK) stock is little changed this year despite phenomenal performance across the board. The market is sensing risk here, but is the apprehension overdone? Let’s see if Carnival stock is really too risky, or if the stock is undervalued.

Cruising along at high speed

Carnival has had a fantastic rebound from what might be called even lower than rock bottom. It’s reporting record highs on several areas of its business, and it just keeps getting better.

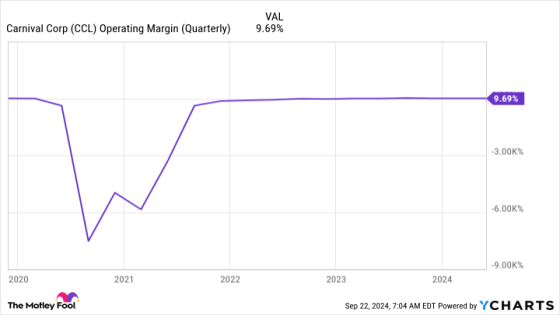

Revenue in the fiscal 2024 second quarter (ended May 31) was a period record of $5.8 billion with record second-quarter operating income of $560 million. Operating margin was about the same as pre-pandemic levels.

It came into 2024 in its best-ever booked position, and that’s continuing through the second half of the year. On top of that, its booked position for 2025 is even better than 2024 so far in both price and occupancy. It’s taking action to meet high demand, and it recently closed out an Australian cruise line to create more availability on some of its most popular routes. It’s already launching cruise dates on new lines through 2027.

It may look like this must come to an end at some point, but it recently got a boost, with the Federal Reserve lowering interest rates. That’s a move that would benefit the economy in general and many companies, especially those dependent on consumer discretionary spending. Its impact is likely to be positively felt by Carnival. While some of its guests are regular travelers, many people save up for a cruise, a one-time affair that’s a lifetime highlight. With easier access to capital, more people will be able to afford their dream cruise trip.

If the elevated demand does eventually taper off, Carnival is likely to be in a stable position and be able to pull off a soft landing.

Carrying a heavy burden

Having no revenue meant a lot of borrowing to keep its doors open for the months it couldn’t sail during the lockdowns. Most of that debt is still on its books, to the tune of $29 billion.

During the past 15 months, Carnival has prepaid $6.6 billion in debt. That knocks out a significant portion of the burden and also cuts debt-service costs. Management envisions paying the debt with its increasing cash from operations, which was $2 billion in the second quarter. It ended the quarter with $4.6 billion in liquidity, so it isn’t under severe financial strain at the moment while it’s paying down the debt.

Another way lower interest rates will benefit Carnival is that it will have an easier time paying off its debts. It’s likely to refinance at lower rates, taking some of the edge off of its high debt. That could mean it will pay it down even faster.

Carrying a valuation that might be ridiculously cheap

The market is pricing in Carnival’s debt to a high degree. Carnival stock trades at a forward P/E ratio of less than 12, and a price-to-sales ratio of just above 1. Those are the kinds of valuations usually seen on low-potential or high-risk stocks.

Carnival, though, is an industry leader with plenty of cash and an excellent business. It has tons of long-term potential.

The worry is that demand slows before Carnival is out of the woods with its high debt. Then it’s stranded in a difficult position with little means to get out of it. It doesn’t have much room for unforeseeable disasters.

It already had a hiccup this year when it had to reroute some lines after the Baltimore bridge collapse. That was good practice to see how well management can deal with challenges and how they could affect Carnival’s financials. The good news is, while there was an impact, it was minimal.

Is Carnival stock too risky? For the highly risk-averse investor, probably. But for most investors, it looks like an opportunity to buy on the dip.

Should you invest $1,000 in Carnival Corp. right now?

Before you buy stock in Carnival Corp., consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Carnival Corp. wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $710,860!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.

Is Carnival Stock Too Risky? was originally published by The Motley Fool

Source Agencies