Most investors who buy Altria Group (NYSE: MO) stock aren’t doing it in hopes of enjoying explosive share price gains. The stock has underperformed the S&P 500 for years. But the dividend? That’s another story. Altria is a world-class dividend stock with a massive yield and a track record of payout hikes spanning more than five decades.

The Dividend King has shown some life this year. This month, the stock climbed above $56 to its highest price since early 2022 before retreating to around $50.

That pullback could make this a perfect buying opportunity for dividend-hungry investors looking for double-digit percentage annual investment returns.

Slow. Steady. Reliable.

Many investors view tobacco companies as the old guard of the stock market. U.S. smoking rates have declined for decades, and it’s widely known how terrible tobacco use of any kind is for one’s health. Altria, which sells cigarettes, chewing tobacco, and smokeless nicotine products in the United States, still gets the vast majority of its revenue and earnings from selling cigarettes. Marlboro is Altria’s flagship brand.

But even today, people seemingly underestimate how resilient the tobacco industry is. The addictive nature of nicotine and high regulatory barriers to new industry entrants has allowed Altria to steadily raise its prices per pack, more than offsetting the fact that Altria sells fewer cigarettes each year.

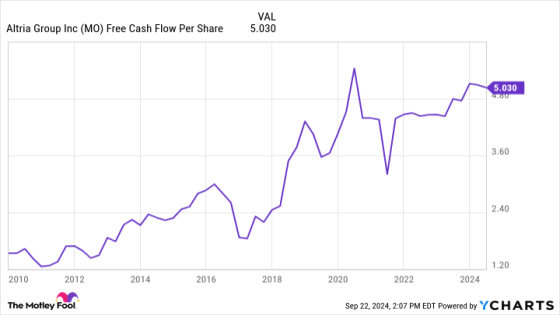

The combination of those price increases and the company’s share repurchases has been enough to generally increase Altria’s free cash flow per share.

Nobody will mistake Altria for a high-growth business. Its earnings grow at low-single-digit percentage rates. The bottom line is that it continues to deliver slow and steady growth. Will that continue forever? Nobody can know for sure. However, there are no signs that it will stop soon. Analysts estimate Altria will grow earnings by just over 3% annually for the next three to five years.

This is no yield trap

A company’s management team may be able to choose how much it pays in dividends, but it can’t entirely control its dividend yield, because that depends on the stock price too. Sometimes, high yields can tempt investors — they can look like easy money. However, a stock’s dividend yield could be high because the market believes the company can’t afford to maintain its payout at previous levels, or because other red flags drive down the share price.

In that context, high-yield stocks can prove to be bad investments, especially if the company cuts its dividend. Such low-quality stocks with high yields that are headed for payout cuts are sometimes called yield traps.

Altria’s dividend yield is high because its earnings grow slowly. The market knows that most of the returns on the stock will come from dividends, and the share price reflects that. Yet Altria is no yield trap because its payout is safe. The company routinely spends about 80% of its earnings on dividends.

That’s a higher dividend payout ratio than most companies, but Altria’s business requires little investment. It can’t even advertise due to tobacco laws. That unique business model allows Altria to comfortably distribute more of its profits as dividends than most companies.

Market-beating investment returns are possible

Altria has been around for generations and is one of the greatest-performing stocks ever. However, it has underperformed the S&P 500 for years now. Yet it could become a market-beating stock again.

Thanks largely to the artificial intelligence trend, the S&P 500 has enjoyed a stellar 31% rally over the past year and trades at a price-to-earnings (P/E) ratio of 24, well above its historical average. While attempting to time the market tends to be a losing strategy, there could be more volatility in the future, and if a U.S. recession occurs, that could trigger a market downturn.

Meanwhile, Altria has a pretty straightforward path to double-digit annualized investment returns. Based on its current 8.1% dividend yield and the expectation for 3% to 4% annualized earnings growth, it could generate a return of between 11% and 12% annually. With a P/E ratio under 9, Altria’s valuation is reasonable enough that investors are less likely to see a further dramatic decrease in the stock’s valuation. Now that the Federal Reserve has begun cutting interest rates, the market may even support higher valuations for high-yield stocks like Altria.

Altria stock can offer reliable dividends and even surprise investors with its total return potential. Its slow growth means investors shouldn’t overpay for the stock, so its recent dip offers a perfect opportunity to add shares while the stock price still makes sense.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $712,454!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Time to Buy the Dip on This 8.1% Hyper-Yield Dividend King? was originally published by The Motley Fool

Source Agencies