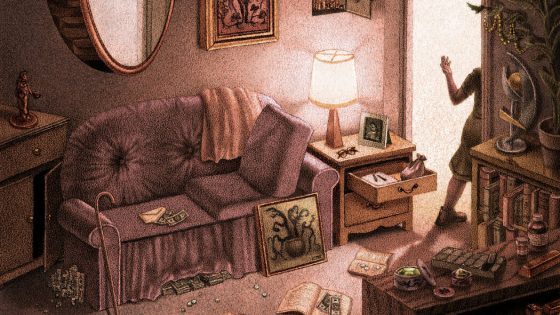

After their father died in 2021, Susan Camp and her brother cleaned out his home — and inadvertently threw out $5,000 in cash he had wrapped in aluminum foil and stashed in the freezer. (Luckily, they later retrieved it.)

And she was surprised, but not shocked, to also discover $6,000 in a box that once held a bottle of cologne. “Dad traveled, and he always wanted cash on him,” she said.

Adrienne Volpe’s grandmother kept her extra cash in her library.

“My grandmother had pressed thousands of dollars in single bills inside books,” Ms. Volpe said. “We thought we were going to find fall leaves” between the pages, she said. They had to open every book in the house to find the cash she had hidden — around $10,000, it turned out, in denominations as small as $20.

It might not be under the mattress, but for people who stumble across a small fortune after an elderly relative dies or moves to a nursing home, uncovering such unexpected wealth — technically part of a person’s estate — can bring complications and even conflict.

Oftentimes, members of older generations perceive keeping cash, gold or other valuables at home as safer than keeping them in a bank, experts say. “I think this is more common for the baby boomer generation and older,” said Mark Criner III, senior trust strategist for Baird Trust in Scottsdale, Ariz. “When you get to that generation, there was a real mistrust of financial institutions,” he said, referring to people old enough to remember the Great Depression and the bank failures of the 1930s.

Mr. Criner said that if family members noticed this behavior, communication was important. “When that’s being recognized, it’s important to start the dialogue,” he said.

What could go wrong?

While throwing cash in the trash is a very real risk of keeping money at home, it is far from the only one, advisers say. Valuables kept in the home can be stolen, destroyed by a disaster like a fire, or surreptitiously appropriated by a family member.

“Things have a way of disappearing from the home, especially when you have existing family drama or a dispute,” said Alvina Lo, chief wealth strategist at Wilmington Trust, a subsidiary of M&T Bank.

This potential for tension among survivors can arise even if no misappropriation takes place, experts say.

“Oftentimes, even if there’s a well-intentioned adult child who lives close by and assets are found, there’s a lot of skepticism that may arise between siblings,” said Abbey Flaum, principal and family wealth strategist at Homrich Berg, a wealth management firm in Atlanta.

People who keep cash at home lose the considerable wealth generation that can take place over decades if that money were invested.

“The lost interest — it probably would have been double, just by having it in the bank all these years versus having it in the bottom of a closet,” said Patrick Simasko, an estate lawyer in Mount Clemens, Mich., who recalled finding close to half a million dollars in cash and gold in the home of an older client who had hired him to execute her estate.

There are also potential pitfalls when it comes to distributing those assets.

“It’s just messy, it’s unofficial and it can lead to accounting nightmares,” Mr. Criner said.

Since cash has no ownership records, “It’s very unclear from a property rights perspective who it belongs to,” Ms. Lo said.

Without a paper trail establishing ownership or a detailed will, determining inheritances can be difficult. “I’ve seen it when you have second marriages, where this can be a problem,” Ms. Lo said, particularly since hidden valuables are unlikely to be accounted for in a will or estate plan.

Experts also say that such unaccounted-for valuables can cause a headache for affluent families, particularly those whose estates are near the threshold of either the federal estate tax, or state taxes on estates or inheritances.

“If it’s on the borderline, those assets might push the estate up to a taxable estate,” said Neil Carbone, trusts and estates lawyer and partner at the law firm of Farrell Fritz. (For 2024, the federal estate-tax exemption is roughly $13.6 million, meaning that estates valued below that level are not subject to taxes; some states have estate taxes or inheritance taxes with lower thresholds.)

Mr. Carbone said he advised clients who inherit valuable but illiquid items, such as artwork, to have them appraised. Establishing the item’s value at the time when the owner died and the inheritor assumed ownership can be important, particularly if the item in question became considerably more valuable over the years.

The Internal Revenue Service has any number of ways to track down potentially taxable wealth, Mr. Carbone said. Auditors might evaluate a homeowner’s insurance policy to look for riders to insure valuable items, conduct a look-back at previous gift tax returns to establish a paper trail of ownership, or trace purchases of precious metals.

The other challenge with inheriting noncash valuables is finding a buyer. “That’s the same thing if you’re investing in baseball cards or Hummel figurines or stamps,” Mr. Simasko said. “If you’re investing in a nontraditional type of investment — not stocks, bonds or mutual funds — you have to find a buyer for them.” This process can take considerable time if the items are especially esoteric, Mr. Simasko added, recalling a client whose wealth was tied up primarily in a collection of antique guitars.

Triggers for cash-stashing

Professionals in wealth management and estate planning say they see cash-hoarding tendencies most often among people with ties to the Great Depression. But memory-robbing medical conditions such as dementia and Alzheimer’s can trigger a reversion to decades-old behaviors, such as cash-hoarding. They may also cause paranoia, which can prompt people to hide valuables and try to block relatives from interceding in their financial affairs on their behalf.

“People who are experiencing this mental diminishment become the least trustful of the people who are the most close to them, and who are in the best position to advocate for them,” Mr. Criner said.

“It can be really difficult. We’ve done lots of planning for clients who could tell Mom or Dad was starting to slip a little bit,” Ms. Flaum said. She said she recommended that clients in this situation obtain a financial power of attorney and consider establishing a revocable trust, a financial instrument where assets can be held as people age and that allows beneficiaries to avoid probate after death.

“A revocable trust is a really good way to plan for management of assets in the event of incapacity,” she said. “You can build in provisions regarding how incapacity may be determined for managing those trust assets.”

Hiding wealth at home has also tended to persist over the years among certain groups of people.

“Particularly, minority communities were very mistrustful of or didn’t have access to financial institutions, which led to the proverbial cash under the mattress,” Mr. Criner said.

“That’s borne of minorities’ lack of access to these institutions for decades, and even when there was access, there was a lot of abuse,” he said. “They weren’t always treated fairly or dealt with honestly.”

These memories linger, Mr. Criner said, adding that, as a Black man, he has heard these attitudes expressed even within his own family. “That sense of distrust goes down from one generation to the next. I’ve heard my dad speak of this, I’ve heard my granddad speak of it,” he said.

Ms. Lo of Wilmington Trust said she has had similar personal experiences. “A lot of this is very cultural, too,” she said. “I’m Asian American, and this happens all the time in my community.”

Over time, experts predict that people’s keeping cash at home will diminish as the collective memory of the Great Depression fades, and the use of digital banking continues to increase.

“People tend to do more and more of electronic payments for things,” Mr. Carbone said.

While this is good news from a financial-planning perspective, people who have seen this dynamic play out say it would also spare survivors the painful emotions these discoveries can cause.

Finding, for instance, hundred-dollar bills secreted amid items that would normally be donated or discarded is stressful for surviving loved ones because it necessitates a much lengthier, painstaking process of removing personal effects from a home. “The families are grieving and it’s very hard for them,” said Ms. Volpe, who is a real estate broker in Hyde Park, N.Y.

Despite a decades-long career in real estate, Ms. Volpe said she hadn’t expected to discover this scenario within her own family. She credited her mother with deducing that more money had been stashed in her grandmother’s books than met the eye.

“Thank God my mother thinks like that,” she said, admitting, “I would have thrown all those books in the garbage.”

Source Agencies