Investors were all over Chipotle (NYSE: CMG) before its huge 50-to-1 stock split earlier this year. Right before the split, Chipotle shares were up 40% year to date (YTD) and crushing the S&P 500 index. Now, with the hype around the split fading and weak guidance in its second-quarter earnings report, shares of the stock have fallen around 25% from all-time highs set in June.

Chipotle is a fast-growing restaurant chain with a loyal customer base, but it still trades at an expensive-looking valuation. Is the stock-split stock a buy after its 25% drawdown? Let’s find out.

Strong comparable sales, weak guidance

In Q2 2024, Chipotle put up more strong results. Revenue grew 18% year over year to $3 billion. This was driven by new store openings and strong comparable sales growth — measuring growth at existing locations — of 11.1%. Restaurant-level margins improved to 28.9%, which shows the operating leverage Chipotle is achieving as it scales its fast-casual Mexican concept.

All this led to earnings per share (EPS) growing by 32% year over year in Q2, an impressive result by any measure. Over the last 10 years, Chipotle has grown its EPS by close to 300%. This growth accelerated during the COVID-19 pandemic’s height and in recent quarters as it has taken market share from other restaurant chains.

So why did Chipotle stock fall after earnings? Because management put out weak comparable sales growth guidance. For the full year, management is expecting comparable sales growth in the mid- to high single digits, which likely means 6% to 9%. In June and July, it has seen comparable sales growth slow down to 6%, which is a big change from the 11.1% in Q2. Management said Q2 had some one-time benefits, including the launch of a temporary popular menu item. Investors were probably disappointed that growth is expected to slow in the coming quarters.

Can earnings keep growing this quickly?

With comparable sales growth slowing down, Chipotle will likely not grow its EPS at a 32% rate over the next five years. That is a high bar. However, I think there is reason to believe it can grow at a 15% to 20% rate without much change to the overall Chipotle business model.

Revenue should be able to grow over 10% due to comparable sales growth and more unit growth. Chipotle has roughly 3,500 locations and believes it can hit 7,000 locations just in North America before reaching market saturation. Add in some margin expansion — something the company has proven time and time again — and underlying earnings can grow even faster. Don’t forget share repurchases, either. The company is now consistently repurchasing stock and has declined its shares outstanding by 11.7% in the last 10 years.

As a per-share metric, EPS will grow faster than underlying net income if shares outstanding continue to decline.

The stock is still not cheap

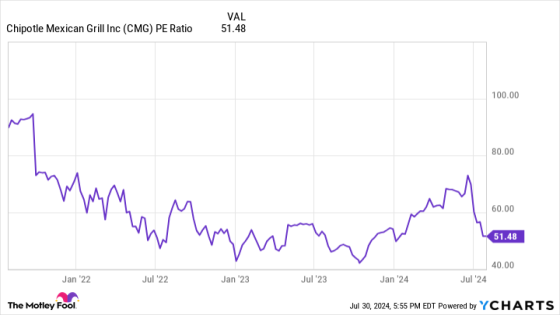

So, it is clear that Chipotle can grow its EPS at a 15% rate for the foreseeable future. That does not necessarily make the stock a buy, though. Today, Chipotle still trades at a price-to-earnings ratio (P/E) of 53. If trailing EPS of approximately $1.021 grows at 15% for the next five years, the metric will double to $2.05.

Compared to the current share price of $52.57, that means Chipotle’s five-year forward P/E is 26. A trailing P/E of 26 is not cheap, let alone a P/E five years in the future. For this reason, Chipotle stock still does not look like a buy after its 25% price dip. Avoid this fast-growing restaurant stock on valuation concerns. Keep it on the watchlist for now.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $18,910!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,544!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $330,931!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of July 29, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends the following options: short September 2024 $52 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

Chipotle Stock Has Fallen 25%: Should You Buy the Stock After Its Historic Stock Split? was originally published by The Motley Fool

Source Agencies