I’d be putting it lightly if I said it has been a roller coaster ride for DraftKings‘ (NASDAQ: DKNG) stock since its July 2019 initial public offering (IPO). After its IPO, the stock surged by over 600% in less than two years, and now it sits around 55% below its peak.

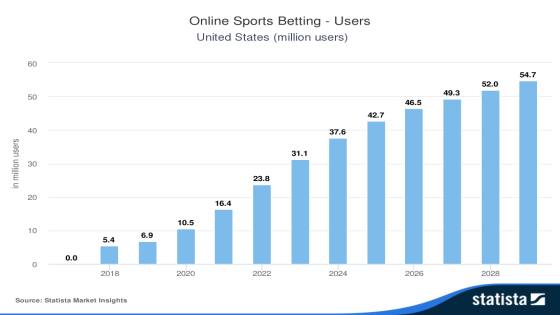

Despite the ups and downs (which is normal for young growth stocks), I still believe in DraftKings’ long-term potential. The business is solid, and it’s operating in a rapidly growing market, as the following chart shows.

The U.S. Supreme Court opened the door for sports betting legalization to states in May 2018, and since then, the number of online sports betting (OSB) users has skyrocketed. If the projections for OSB users are accurate and an estimated 17 million more users join the platform over the next five years, DraftKings is well-positioned to continue its positive momentum.

DraftKings’ customer acquisition momentum has been going strong

Of course, not all of the projected new OSB users will be going to DraftKings’ platform. But if recent user growth indicates DraftKings’ potential, the platform should attract many of these new users.

At the end of the second quarter, DraftKings had 8.4 million unique users in the past 12 months. That’s 900,000 more than in the first quarter, and 2.2 million more than just one year ago. Five years ago, in Q2 2019, this number was just 1.8 million, so it’s safe to say DraftKings has been on an impressive growth trajectory.

With the number of OSB platforms growing, attracting new users has become increasingly competitive. However, DraftKings was able to reduce its customer acquisition cost by over 40% year over year. The company’s CEO said he anticipates this “healthy customer acquisition environment” to continue through 2024 and beyond, possibly highlighting that the U.S. OSB market is larger than anticipated.

DraftKings is playing the long game

In Q2, DraftKings’ average revenue per monthly unique player (ARPMUP) was $117, down from $137 in Q2 2023.

While it’s not ideal that ARPMUP is decreasing, much of this can be attributed to its Jackpocket acquisition, which added more users to account for. In this growth stage, acquiring users and market share is a higher priority than maximizing profits (although that’s also important), and DraftKings is focusing on that.

The company continues to invest in customer acquisition and retention, aided by impressive revenue growth that gives it the financial backing to support these initiatives.

In Q2, DraftKings generated $1.1 billion in revenue, up 26% year over year. This impressive quarter caused it to raise its 2024 revenue guidance to $5.05 billion to $5.25 billion, up from the previous $4.8 billion to $5 billion range it estimated. This would work out to year-over-year growth of between 38% to 43%.

A short-term risk to its customer acquisitions and retention

An interesting move from DraftKings involves how it plans to handle high taxes in select states. Starting Jan. 1, 2025, the company will implement a “gaming tax surcharge” in four states with tax rates above 20% and multiple sports betting operators: Illinois, New York, Pennsylvania, and Vermont.

I imagine most users in those states aren’t happy to hear this, and there’s a risk of losing them to other platforms, but it’s a means to an end for DraftKings. The company expects this move to considerably increase its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), which it expects to be between $900 million and $1 billion in 2025 without the gaming tax surcharge.

DraftKings will probably receive a lot of criticism for this move, but it wouldn’t be surprising if other platforms followed suit after seeing how users react and seeing the financial effect.

Should you invest $1,000 in DraftKings right now?

Before you buy stock in DraftKings, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DraftKings wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $606,079!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

Stefon Walters has positions in DraftKings. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Despite Being Down 55% From Its Peak, Here’s Why I’m Loading Up On This Growth Stock was originally published by The Motley Fool

Source Agencies