While there is technically no such thing as a “bulletproof” stock, there are a select few businesses that seem almost unstoppable. Combining incredible historical total returns with robust returns on invested capital (ROIC) and steadily rising dividends, some companies are built to stand the test of time.

Four such businesses are Costco Wholesale (NASDAQ: COST), Cintas (NASDAQ: CTAS), Rollins (NYSE: ROL), and Badger Meter (NYSE: BMI). Delivering total returns between 2,810% and 12,100% since 2000, these stocks look as bulletproof as anyone can imagine. Thanks to this history of success and the companies’ powerful businesses, each stock trades with a price-to-earnings (P/E) ratio between 53 and 56 — double that of the S&P 500‘s average.

Still, here’s why these four stocks are perfect for keeping on your radar in the event of a sell-off or for buying via dollar-cost averaging (DCA) over an extended time frame.

1. Costco Wholesale

Had an investor bought $100 worth of Costco shares at the company’s initial public offering (IPO) in 1985 and held until today, they would now have over $150,000. Quickly growing to become the world’s third-largest retailer, Costco is home to 876 warehouses and roughly 134 million cardholding members.

Laser-focused on streamlining its operations to provide products and services at the lowest cost possible, the company generates over $4.4 billion in membership fees annually from value-oriented consumers. Powered by this membership model, paired with Costco’s careful curation of its (mostly) buy-in-bulk product assortment, the company has trenched a wide cost advantage moat around its ever-streamlining operations.

In addition to this cost advantage moat, the company also has a brand loyalty moat, thanks to the fact that consumers are willing to pay a $65 annual fee just for the privilege of shopping there. Further adding to this brand power, Costco saw a 93% renewal rate among its U.S. and Canadian members (and a 90% rate from its international members), demonstrating an incredibly loyal customer base.

Stock-wise, Costco’s rising ROIC of 24% hints at the potential for continued outperformance, especially as management expects to continue growing its warehouse count by 3% to 4% annually for the foreseeable future. With sales, net income, and dividends growing by 9%, 12%, and 13% annually over the last decade, Costco will probably deliver near-perfect earnings, as usual, on Sept. 26.

But if it doesn’t, I’ll be ready to add.

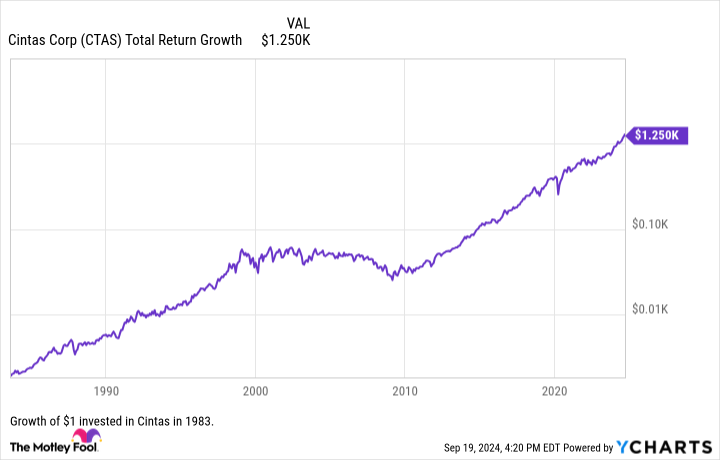

2. Cintas

Cintas provides many of the core essentials needed for businesses to function, including uniforms, restroom supplies, floor care, first aid equipment, fire extinguishers, and a wide array of safety equipment and training. While these operations aren’t exactly exhilarating, the fact that Cintas has become a 1,250-bagger since its 1983 IPO is.

Growing sales and adjusted earnings per share (EPS) in 52 of the last 54 years, Cintas is as bulletproof as any stock can be. Generating 70% of its sales from customers in services sectors (healthcare, hospitality, and dining, for example) and 30% from producers (such as manufacturing and construction), the company serves a diversified base of over 1 million customers.

Despite growing its sales by more than 1,000-fold over the last four decades, Cintas believes there are more than 15 million businesses in North America that don’t yet use its products. This fact leaves Cintas with a long growth runway ahead as it continues to whittle away at the heavily fragmented industry it serves.

Delivering sales, net income, and dividend growth of 9%, 19%, and 27% annually over the last decade, Cintas and its ROIC of 24% are showing no signs of weakness, making future dividend increases almost certain.

3. Rollins

While Rollins has “only” recorded total returns of roughly 13,000% since 1989 (it’s tough to beat Cintas and Costco’s ridiculous figures), the company has more than quadrupled the S&P 500’s mark over the same time. Ascending to become North America’s largest pest control business, Rollins has proven to be one of the most resilient companies of the 21st century.

Emphasizing this point, during the 2008 financial crisis, the industrial slowdown in 2015, and the pandemic in 2020, Rollins delivered sales growth of 6%, 6%, and 12%. One reason for this success during challenging times is the company’s history as a serial acquirer. By maintaining a pristine balance sheet alongside ever-improving profitability, Rollins loves to pounce during rough macroeconomic periods and pick up dozens of its smaller peers in the highly fragmented pest control industry in one fell swoop.

This heavy merger and acquisition (M&A) strategy works because the company has proven to be a top-tier integrator once it adds these new businesses — as evidenced by its impressive 30% ROIC. Comparing Rollins’ profitability to its debt and equity, this high ROIC shows that the company is a masterful acquirer.

Generating sales, net income, and dividend growth of 9%, 14%, and 15% annually over the last 10 years, Rollins is another excellent investment to monitor for a dip in price or to add to slowly with DCA purchases.

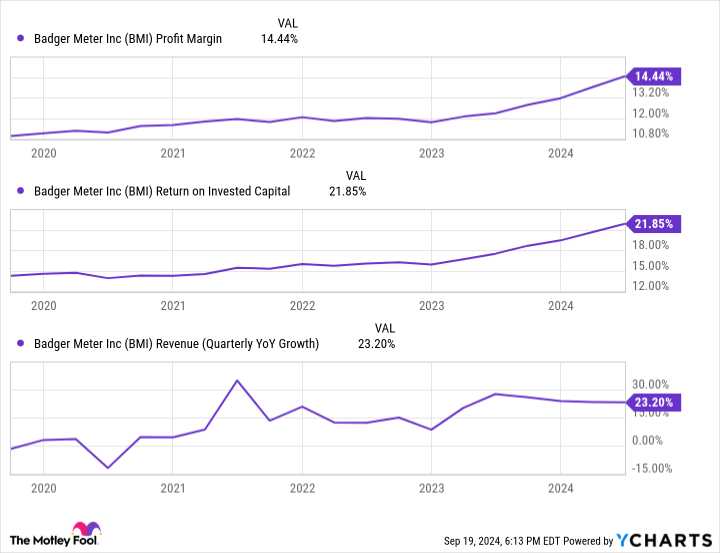

4. Badger Meter

Although leading water solutions provider Badger Meter has delivered total returns of over 43,000% since 1972, the company’s most promising days may still be ahead. Thanks to its BlueEdge suite of solutions that “integrate water technology, software, and services for the management of water,” Badger Meter has become a force in the $20 billion smart water industry.

While the company offers basic instrumentation like meters, valves, and sensors, its bleeding-edge advanced metering infrastructure is what will really drive the stock’s performance from now on. Providing connectivity and communication solutions to water utilities, Badger Meter brings the largely outdated industry into the modern era, enabling live insights that lead to immediate action.

This real-time analysis is quickly becoming a must-have for Badger Meter’s customers due to rising compliance standards and the world’s heightened focus on water conservation. Not only has this booming smart water industry been a boon to the company’s sales growth, but it has also helped boost the company’s profitability and ROIC, as these tech-heavy solutions have much higher margins.

Growing sales and EPS by 23% and 49% in the first half of 2024, Badger Meter’s reinvigorated growth story has me optimistic that the company is on track to become a Dividend King in 2043.

Should you invest $1,000 in Costco Wholesale right now?

Before you buy stock in Costco Wholesale, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Costco Wholesale wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $710,860!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

Josh Kohn-Lindquist has positions in Badger Meter, Costco Wholesale, and Rollins. The Motley Fool has positions in and recommends Costco Wholesale and Rollins. The Motley Fool recommends Cintas. The Motley Fool has a disclosure policy.

4 Bulletproof Dividend Growth Stocks I’d Love to Buy After a Dip in Price was originally published by The Motley Fool

Source Agencies