Those who put $10,000 in the initial public offering (IPO) of coffee company Starbucks (NASDAQ: SBUX) more than 30 years ago are millionaires today. In short, this has been an absolutely magnificent Nasdaq growth stock. However, this magnificent growth stock is now down more than 40% from its all-time high in 2021, which is one of the worst (and longest) pullbacks the stock has ever experienced.

In hindsight, the impending pullback for Starbucks stock should have been obvious. After all, when it hit an all-time high in 2021, the stock was also trading at a decade-high price-to-sales (P/S) valuation of 6 — that was easily 50% to 100% more than what was normal for this company, suggesting shares were overvalued at the time.

Starbucks stock has dropped, in part, because it was overvalued at one point. That said, the company isn’t doing itself any favors right now. Underperformance in China in recent years — its second-biggest market — has led to a lower net profit margin than what it had a decade ago.

More recently, operations in the U.S. have stumbled. Starbucks reported financial results for its fiscal second quarter of 2024 on April 30, with the stock further plunging as a result. Former longtime CEO Howard Schultz was quick to offer his thoughts on social media. According to Schultz, “U.S. operations are the primary reason for the company’s fall from grace.”

But is Schultz right? It could make all the difference for Starbucks’ shareholders now.

The one thing Starbucks needs to fix right now

Investors might be able to debate whether U.S. operations are the primary reason for Starbucks’ “fall from grace.” But U.S. operations are certainly a contributing factor.

Consider that Starbucks ended Q2 (which ended March 31) with over 18,000 North America locations, which was a 3% increase from the prior-year period. However, North America revenues were completely flat despite the company having more stores. The reason for this is that same-store sales fell by 3%, pulled lower by a stunning 7% drop in transactions.

Unfortunately for Starbucks’ shareholders, the company can only blame itself for this huge decrease in transactions. It’s simply not running its stores well.

For evidence, consider what Starbucks’ management had to say about its order completion rate. The company has over 33 million rewards members using its app, and these are some of the brand’s most loyal fans — they account for a whopping 60% of sales in the morning. Many place orders through the app and pick up in the store. However, these fans are increasingly frustrated.

Starbucks’ customers are tired of waiting a long time for their orders and are frustrated that items that they want aren’t in stock. These customers are placing orders through the app. But increasingly, they aren’t picking them up because they’re tired of waiting for what they want.

In other words, if Starbucks was merely operating efficiently or had items properly stocked, then it probably wouldn’t have had a drop in transactions. The problem wasn’t consumer demand; the problem was failing to meet the demand in a timely fashion.

Because of unprofitability in other parts of the business, Starbucks’ operating income for North America alone exceeds its total operating income, showing just how important this region is to the overall business. And operating income in North America dropped 6% year over year in the second quarter primarily due to the loss of operating leverage from lower sales per location.

What if Starbucks solves this problem?

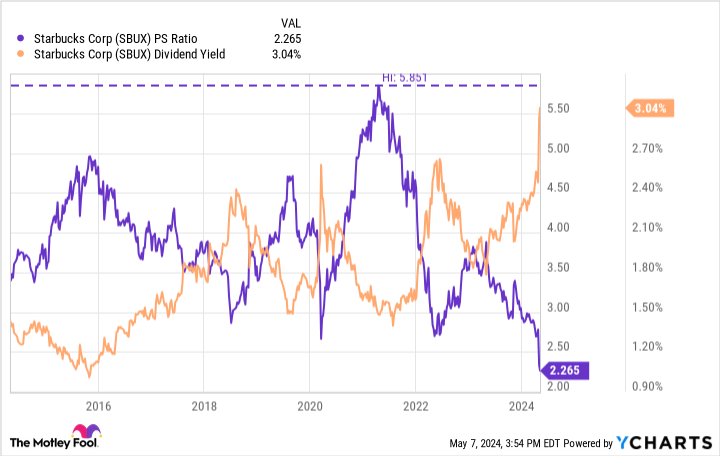

Starbucks was due for a pullback due to its high valuation. But the stock has continued falling due to self-inflicted operational struggles. Shares now trade at their lowest valuation in over a decade, with a reasonable P/S ratio of just 2.3. Moreover, the stock’s dividend yield is over 3% for the first time.

In other words, from a valuation perspective, Starbucks stock hasn’t been this attractive in years. However, the attractiveness of the investment is predicated on management’s ability to fix its problems.

There’s reason for skepticism. Starbucks CEO Laxman Narasimhan has been on the job for only one year, so this isn’t the same management team that oversaw huge gains for Starbucks stock. And it seems that Narasimhan sees the company’s problem differently than former CEO Schultz.

For his part, Narasimhan told CNBC that Starbucks didn’t “really attack the occasional customer with delivering and communicating value to them in a more aggressive manner.” In other words, he seems to think the company needs to attract nonloyal customers with bargains, not give loyal customers what they want quicker.

Starbucks might slow progress by misdiagnosing the problem, which would be frustrating for investors. But consumers really love this brand and the company has recovered from missteps before, so there’s reason for optimism as well.

Those who invest now can enjoy a nice dividend while they wait for results, which I think tips the scales toward buying Starbucks stock today.

Should you invest $1,000 in Starbucks right now?

Before you buy stock in Starbucks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Starbucks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Jon Quast has positions in Starbucks. The Motley Fool has positions in and recommends Starbucks. The Motley Fool recommends Nasdaq. The Motley Fool has a disclosure policy.

This Magnificent Nasdaq Growth Stock Is Down More Than 40% and Trading at a Once-in-a-Decade Valuation. If It Gets This 1 Thing Right, the Stock Could Soar. was originally published by The Motley Fool

Source Agencies